Bonds, Equities & Oil - Latest Thoughts

Bonds, Equities & Oil - Latest Thoughts

Below is a round-up of Longview related views/research & trade ideas – this is published most Fridays, and updates key themes and highlights key pieces of (often contrarian) research.

Starting to re-BUILD US Treasury OW (in strategic portfolios)

April has not been good for bonds. The US 10 year yield, for example, is up 50bps MTD (FIG A), while 2 year (+37bps) and 5 year (+49bps) yields are also sharply higher. Consistent with that, investors have dumped bonds this month at their fastest pace in over 20 years (i.e. fastest since July 2003), i.e. according to the BAML fund manager survey (FIG B below).

FIG A: US 10 year Treasury yield (%), with 50, 90, & 200 day moving averages

FIG B: Change in FMS net % overweight to fixed income

Naturally, there’s potential for further upside in yields in coming weeks and months. Markets, though, are forward looking. Once everyone is talking about the key issue of the day (as they are currently), it’s usually already baked in/reflected in the price.

That favours a contrarian approach, particularly when (i) positioning and sentiment become extreme; and (ii) there’s an emerging macro reason to lean against the dominant emotion in markets.

With respect to bonds, we are probably at/close to one of those moments (i.e. when it pays to be contrarian). This week, therefore, we started to re-build OW exposure to US Treasuries in our strategic portfolio, having reduced the OW in December last year.

The rationale is laid out in our latest monthly asset allocation update (see extract below – contact Nick Beazley at nick@longvieweconomics.com for a copy of the full analysis).

Extract from Strategic Asset Allocation note No. 37, 25th April 2024

“Traders Add Bets That Fed Will Skip Interest-Rate Cuts This Year”

Source: Bloomberg article, 23rd April 2024, available HERE

Having sold off sharply since late December, the consensus view on US Treasuries is poor. In particular, inflation is proving to be ‘sticky’ and is viewed as the biggest ‘tail risk’ in markets (on the BAML survey, fig 9); Fed commentary has been hawkish; rate cuts for this year have been largely priced out; while the US economy has performed well/surprised to the upside in 2023 (e.g. with strength in certain headline job data). Some, therefore, are calling for a ‘no landing’ and looking for ‘no Fed cuts’ this year (e.g. see quote above).

Fig 1: Longview medium term technical scoring system vs. US 10y future

Other widespread concerns about long duration Treasuries include (i) America’s large fiscal deficit, high levels of Treasury issuance expected this year/next, and ongoing QT (i.e. sales of Treasuries by the Fed), at a time when the RRP is close to empty. All of which, the bears argue, has the potential to generate a liquidity squeeze in the Treasury market (akin to October last year).

For three key reasons, though, a rally in Treasuries in coming months and in 2H 2024 (and perhaps beyond) is likely. In particular, many of those concerns/factors noted above are backward looking and already in the price. In that respect:

(i) US inflation is not sticky in our view, and should surprise to the downside later this year (point 1);

(ii) a slowdown in the US economy (i.e. mid-cycle ‘soft patch’) is likely in coming quarters (point 2); while

(iii) technical, sentiment, and positioning models point to significant upside in Treasuries (on a 3 – 6 month time horizon, and potentially beyond, see point 3).

Last December, we reduced exposure to US Treasuries (from +9pp. OW vs. our benchmark, to +3pp. OW). That decision reflected SELL signals from a number of key models (e.g. see fig 1), amongst other factors laid out in our December 2023 Quarterly report. Given those three points above, though, the risk reward favours starting to re-BUILD the OW Treasury position (to +6pp. OW), with a corresponding reduction in cash (see tables 1 & 2 for detail). Please see points 1 – 3 below for full analysis.

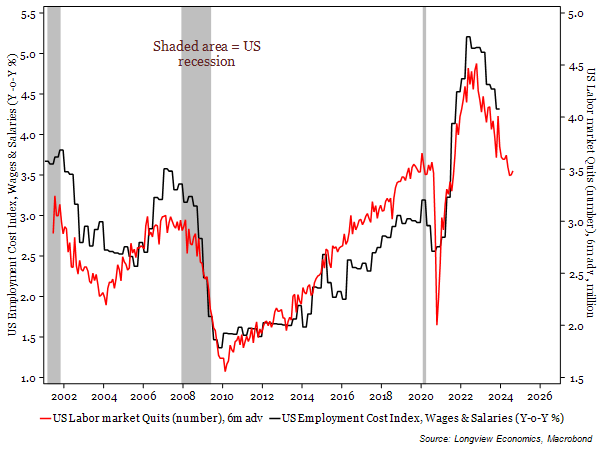

Fig 2: US ECI (wages & salaries, Y-o-Y %) vs. US job quits (number), 6m adv.

Keep reading with a 7-day free trial

Subscribe to The (Long)View From London to keep reading this post and get 7 days of free access to the full post archives.