How Strong is the US Consumer

How Strong is the US Consumer

Recession vs. Soft Landing – Building the Case

“The outlook for thef US economy over the next 6 – 12 months sits at the heart of

almost all key global investment decisions at the moment. Is a recession

imminent, as many claim (see quote)? Or is the economy due a soft landing?

Correctly answering that question will deliver significant outperformance of asset

allocation portfolios, as well as sector and global equity portfolios (& bond, commodity

and other types). Getting the answer wrong, however, will lead to significant

underperformance.”

Source: (Long)View from London, 30th August 2024 “US Macro: Soft Landing or Recession? A.k.a It’s All About the US Macro Call” - see HERE.

Two weeks ago in the (Long)View from London, we wrote about the current heightened importance of the ‘recession vs. soft landing’ macro call, and how most asset prices are poised at key levels, waiting for more evidence to generate a clearer steer on that question (see quote above).

One week ago in the (Long)View from London (i.e. last Friday), we then discussed the idea that “This Time is Different”, highlighting how even though the dis-inversion of the yield curve is signalling an imminent start to the recession, other equally predictive macro indicators are generating the opposite message. The corporate financing gap, for example, is showing that the US corporate sector (as a whole) is free cashflow generative. That is, it’s not overstretched and therefore not likely to cut costs (labour and others) aggressively in the event of soft economic growth. It’s also very profitable, with high margins and low debt levels. All of which points to a robust corporate sector and, therefore, a ‘soft landing’ rather than a ‘recession’.

We also outlined in that piece how the message from the US labour market data is mixed, with a number of indicators behaving well, and therefore not confirming the ‘recession’ expectation. Those included the absence of a high level of Challenger job cuts; the low and currently stable level of weekly jobless claims, as well as the state by state Sahm Rule analysis. That message was reinforced this week with another benign weekly jobless claims data point – see fig 1.

Fig 1: US weekly initial jobless claims (1 & 4 week smoothed)

As such, there are clear conflicting messages about the recession question. Some effective, predictive indicators are signalling an imminent recession. Other equally predictive ones are not. In that sense, this time is different. In a similar manner, opinion amongst economists/market forecasters is divided.

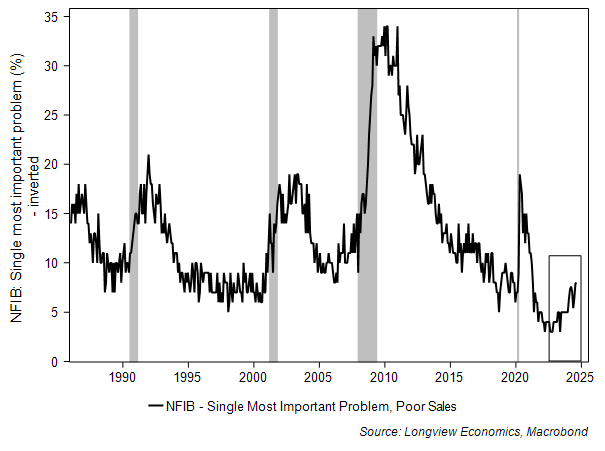

What is clear, though, is that the US economy is slowing. Profit warnings from Ally Financial (auto lender), a slowing trend in NFP employment (since March – see Fig 9 in appendix) as well as a pick up (from low levels) of small businesses mentioning ‘poor sales’ as their ‘single most important problem’ (fig 2) are all highlighting that slowing dynamic.

Fig 2: US NFIB small business survey – single most important problem/sales

Keep reading with a 7-day free trial

Subscribe to The (Long)View From London to keep reading this post and get 7 days of free access to the full post archives.