“How Tight is the US Labour Market? How Sticky is Inflation…..Really?”

“How Tight is the US Labour Market? How Sticky is Inflation…..Really?”

Below is a round-up of Longview related views/research & trade ideas – this is published most Fridays, and updates key themes and highlights key pieces of (often contrarian) research.

Divergent Global Macro Trends

“If our updated assessment of the inflation outlook, the dynamics of underlying inflation and the strength of monetary policy transmission were to further increase our confidence that inflation is converging to our target in a sustained manner, it would be appropriate to reduce the current level of monetary policy restriction.”

Source: Christine Lagarde, ECB press conference, 11th April 2024

The key economic regions of the world are in very different economic states.

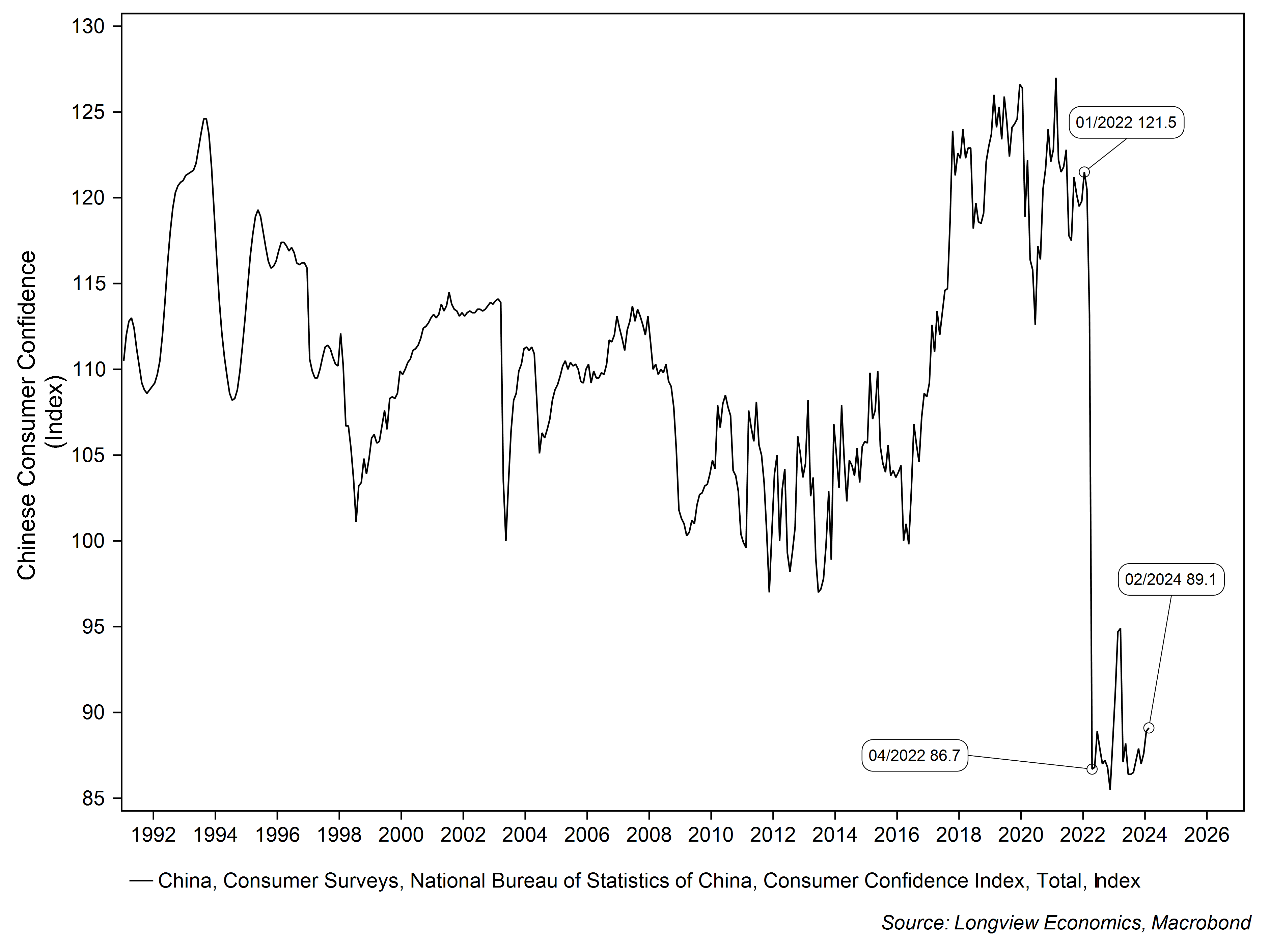

China is in the midst of a balance sheet recession. Its housing bubble has burst. Debt levels are at record highs (and up dramatically in the past 10 – 15 years), while confidence is especially depressed (although just up from record lows). All of that has been weighing on growth (and confidence#), while stimulus has been lacking. Of late some signs of life have been appearing (as we’ve shown in detail previously, contact Nick Beazley at nick@longvieweconomics.com for a copy of the full report). To date, though, the impact of the stimulus has been mixed (e.g. housing remains depressed, some macro data has ticked higher).

FIG 1: Chinese consumer confidence (index)

The Eurozone, meanwhile, is edging toward rate cuts. This week, the ECB and Christine Lagarde as good as confirmed that June is likely to be their first rate cut (see quote above). Underlying inflation pressures, though, are more muted than the ECB care to admit (more on that next week). Growth meanwhile is tracking close to zero.

The UK situation is similar to that of the Eurozone. Growth is at/close to zero, and inflation pressures are dissipating rapidly. As we outlined in our UK macro research earlier this week (contact Nick Beazley at nick@longvieweconomics.com for a copy of the full report, UK inflation is likely to be as low as 0 – 1% later this year. In an economy with no growth, that points to the need for a strong rate cutting response by the BoE.

The US, in contrast, remains the bright spot amongst the major regions of the world. Latest growth expectations, according to the ‘Blue Chip’ consensus are for 2.0% annualised growth (in Q1, 2.4% according to the latest AtlantaFed GDPNow tracker), with that growth rate slowing but remaining positive over the next three quarters. In contrast to the UK, China & Eurozone, inflation remains a concern. ‘Supercore’ has accelerated in recent months, while rising NFIB price plans & ISM manufacturing prices paid surveys, coupled with seemingly tight labour markets, are concerning Fed governors and other economic commentators.

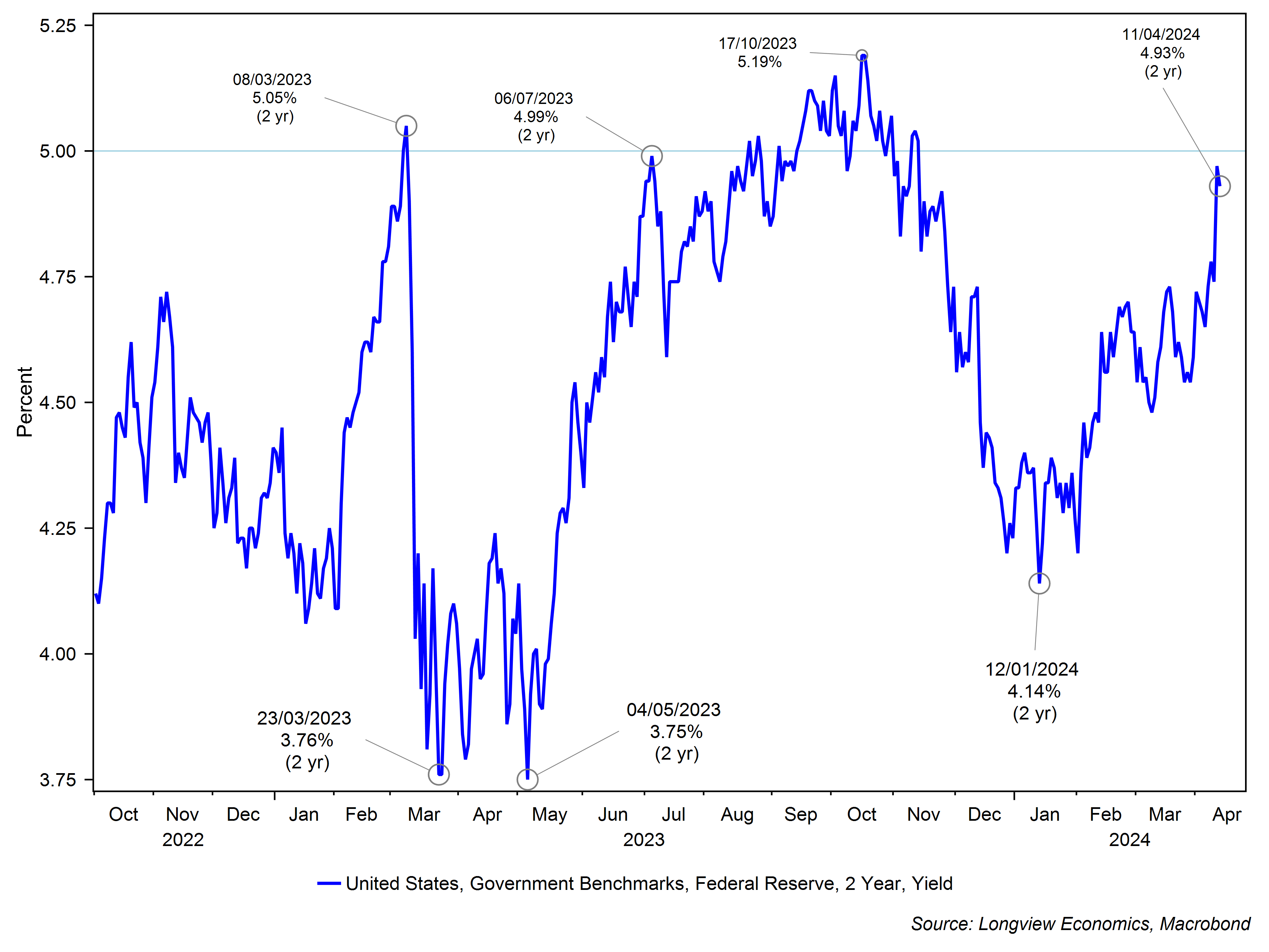

Those concerns have been reinforced by this week’s stronger than expected US CPI data (Wednesday). That, in turn, generated a further pricing out of 2024 and 2025 rate cuts, sharp moves higher in government bond yields across the curve (with US 2 year yields, for example, now back close to 5% - fig 2), and a stronger dollar. The YEN, for example, has broken through its 151 key level (i.e. weakened), while the Euro is at its weakest since November last year.

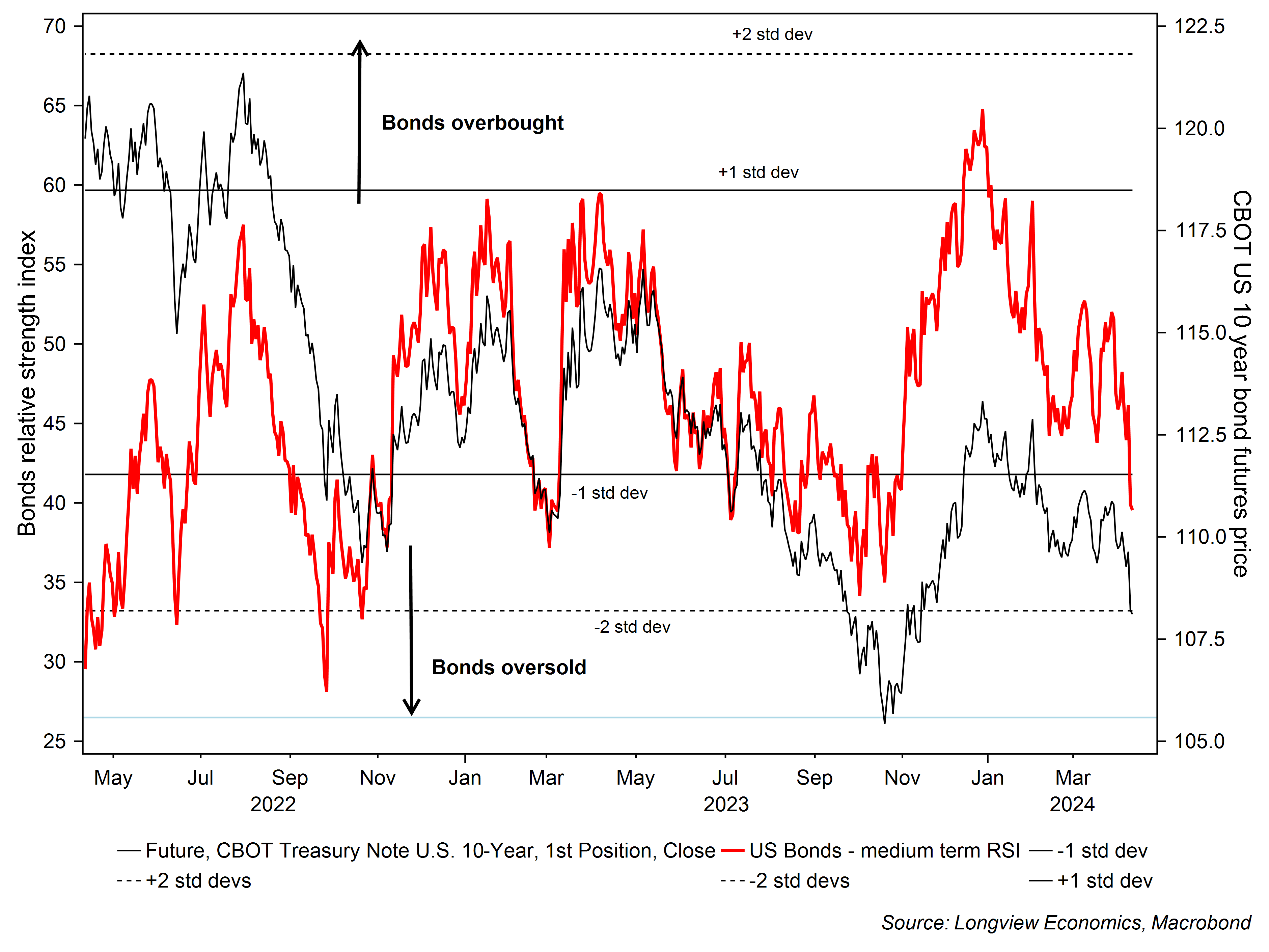

The increasingly one way nature of market concerns (re: US inflation), though, are generating opportunities. Indeed, aside from the impressive resilience of the equity market this year (despite pricing out of rate cuts), US bonds are now oversold. The 10 year yield, towards the end of last year, was as low as 3.79%. As of Thursday’s close, it was yielding 4.56% (and oversold on a medium term RSI indicator – fig 3). US 2 year yields have also backed up sharply (and are now back close to record 2006 highs).

FIG 2: US 2 year government bond yields (%)

FIG 3: Medium term RSI (for US 10 year bond futures) vs. 10 year bond futures

There are, though, two groups of reasons to view those high yield levels as an opportunity.

That is, there are question marks about the extent of the stickiness of US inflation, as well as risks associated with the US growth outlook.

Questioning the ‘Sticky’ Inflation Narrative

Both core and headline CPI were higher than expected in March (published this week). As mentioned above, that had a meaningful impact on various asset prices (although it was notable how resilient both equities and gold have been despite Wednesday’s weakness).

Keep reading with a 7-day free trial

Subscribe to The (Long)View From London to keep reading this post and get 7 days of free access to the full post archives.