The State of Markets

The State of Markets

A brief review of all key upcoming events across the major regions of the globe & an overview of key recent market trends.

The State of Markets: "The Fed -> 50 or 25bps?"

“We are at a point where you might say, ‘I could go either way — 25 or 50,’ but I think the risk management has shifted to the labor market and favors doing 50,” he said.

Source: WSJ, 12th September, “The Fed’s Rate-Cut Dilemma: Start Big or Small?” Nick Timiraos, Sept. 12, 2024

https://www.wsj.com/economy/central-banking/fed-interest-rate-cut-size-861c9600

It’s all eyes on the Fed this coming week as they meet to kick start a rate cutting cycle. The market is split as to whether the first cut will be a standard 25bps cut or a ‘front loaded’ 50bps. On Wednesday, after a slightly disappointing US monthly core CPI print, the market moved away from the likelihood of 50bps next week. By Thursday, however, after an article by Nick Timiraos in the WSJ (see quote above), the probability of 50bps had shifted sharply back into focus. With that, US 1-year bond yields made a new (almost) 2 year low on Friday (along with US 2-year yields), while gold made a new high. Timiraos is widely regarded as a ‘mouthpiece’ for the Fed, who often use his articles to signal their intentions to the market. A similar article appeared in the FT.

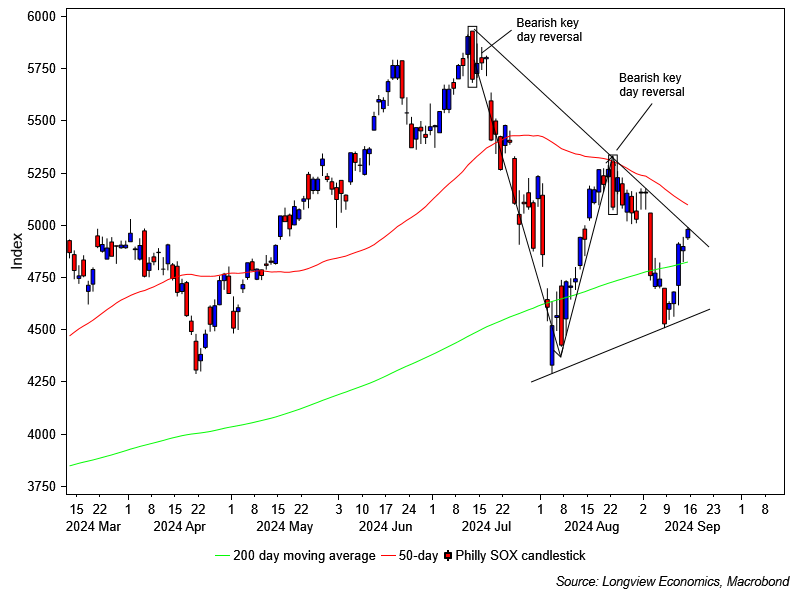

Whilst markets were down at the start of September, they bounced back sharply last week (helped by the increasing chance of 50bps). The S&P500 was +4.0% on the week (after falling by 4.2% in the prior week); the NDX100 was +5.8% (after -5.9% the prior week); while, more dramatically, the Philly SOX index was +10.0% (after -12.2%). With that, some key indices have now generated pennant patterns (e.g. see key chart below). Often that’s associated with indecision in markets, as they ‘tread water’ in a narrowing range (before then breaking out one way or the other).

As well as the Fed decision on Wednesday (along with a press conference and an updated summary of economic projections), there’s also a ‘housing data’ theme in the US, with the release of the NAHB homebuilders’ index (Tuesday); housing starts and building permits (Wednesday); and existing home sales (Thursday). Elsewhere there are monetary policy decisions from both the BoE (Thursday) and BoJ (Friday). Please see below for a full list of key macro data & events

Key chart: Philly SOX cash candlestick, shown with 50 & 200 day moving averages

(All in London time BST)

Events: N/A

Data: N/A

Earnings: N/A

Events: N/A

Data: US retail sales (Aug, 1:30pm); US NAHB homebuilders index (Sept, 3pm).

Earnings: Ferguson.

Events: Fed policy decision (Wed, 7pm).

Data: UK headline & core CPI (Aug, 7am); US housing starts & building permits (Aug, 1:30pm).

Earnings: General Mills.

Events: Bank of England policy decision (Thurs, 12pm).

Data: US Conference Board leading index (Aug, 3pm); US existing home sales (Aug, 3pm).

Earnings: FedEx, Lennar.

Events: PBoC (1 & 5 year LPR) policy decision (2am); BOJ policy decision.

Data: German PPI (Aug, 7am); Eurozone consumer confidence (September first estimate, 3pm).

Earnings: N/A

The SHORT VIEW (& market positioning), 10th September 2024:

“OIL: BUY Case Brewing”

“Last week, the OPEC+ alliance led by Saudi Arabia and Russia decided to delay the unwinding of its production cuts that were planned to begin in October. The first addition to supply, of 180,000 barrels per day (bpd), is now expected for December.”

Source: Oilprice.com article, 9th September 2024

In recent months, asset price volatility has picked up as markets have priced in a growth slowdown in the US economy. Fixed income, for example, has rallied sharply, the rates market has priced in a significant easing cycle from the Fed (~250bps of cuts by late 2025/early ’26); and, with that, key cyclically sensitive commodity prices have fallen to low levels, along with 10 and 30 year US bond yields.

Events: N/A

Data: US Empire manufacturing (Sept, 1:30pm); Canadian existing home sales (Aug, 2pm).

Earnings: N/A

Events: N/A

Data: Canadian housing starts (Aug, 1:15pm); US retail sales (Aug, 1:30pm); US New York Fed services business activity (Sept, 1:30pm); Canadian headline & core CPI (Aug, 1:30pm); US industrial & manufacturing production & capacity utilisation (Aug, 2:15pm); US business inventories (Jul, 3pm); US NAHB homebuilders index (Sept, 3pm).

Earnings: Ferguson.

Events: Fed policy decision & summary of economic projections (7pm); Bank of Canada publishes summary of deliberations (6:30pm).

Data: US housing starts & building permits (Aug, 1:30pm); US total net TIC flows (Jul, 9pm).

Earnings: General Mills.

Events: N/A

Data: US current account balance (Q2, 1:30pm); US Philadelphia Fed business outlook (Sept, 1:30pm); US weekly jobless claims (1:30pm); US Conference Board leading index (Aug, 3pm); US existing home sales (Aug, 3pm).

Earnings: FedEx, Lennar.

Events: N/A

Data: Canadian retail sales (Jul, 1:30pm); Canadian industrial product & raw material price index (Aug, 1:30pm).

Earnings: N/A

Fig B: US Conference Board leading index (Y-o-Y %)

Events: Speeches by the ECB’s Guindos at event VII Foro Banca (9:10am), Lane at European Investment Bank Chief Economists' meeting (1pm) & Panetta in Rome.

Data: Italian core CPI (Aug, 9am); Eurozone trade balance & labour costs (Jul/Q2, 10am).

Earnings: N/A

Events: N/A

Data: German & Eurozone ZEW survey – expectations & current situation (Sept, 10am).

Earnings: N/A

Events: Speeches by the ECB’s Holzmann & Vujcic at Vienna conference (8am & 8:15am) & Nagel in Frankfurt (12pm).

Data: Eurozone headline & core CPI (August final estimate, 10am); Eurozone construction output (Jul, 10am).

Earnings: N/A

Events: Speeches by the ECB’s Knot on global financial outlook, EU monetary policy and financial institutions (8:15am), Nagel in Elmau (12:30pm) & Schnabel on current aspects of monetary policy (10am & 3:40pm).

Data: Eurozone new car sales (Aug, 5am); Eurozone ECB current account (Jul, 9am); Italian current account balance (Jul, 9:30am).

Earnings: N/A

Events: The ECB’s Lagarde delivers Central Bank lecture (4pm).

Data: German PPI (Aug, 7am); French INSEE business & manufacturing confidence (Sept, 7:45am); Eurozone consumer confidence (September first estimate, 3pm).

Earnings: N/A

Fig C: Eurozone consumer confidence (index)

Events: N/A

Data: Rightmove house prices (Sept, 12am).

Earnings: N/A

Events: N/A

Data: N/A

Earnings: N/A

Events: N/A

Data: Headline & core CPI, RPI & PPI (Aug, 7am); Land Registry house prices (Jul, 9:30am).

Earnings: N/A

Events: Bank of England policy decision (12pm).

Data: N/A

Earnings: N/A

Events: N/A

Data: GfK consumer confidence (Sept, 12am); retail sales (Aug, 7am); public sector finances (Aug, 7am).

Earnings: N/A

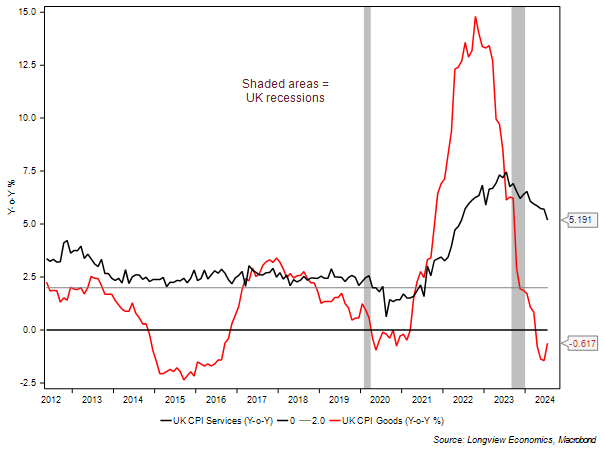

Fig D: UK services & goods CPI (Y-o-Y %)

Events: Market holidays in various APAC countries (e.g. China, Hong Kong, Japan etc.) on account of Mid-Autumn Festival (Mon – Wed).

Data: N/A

Earnings: N/A

Events: Market holidays in various APAC countries (e.g. China, Hong Kong, Japan etc.) on account of Mid-Autumn Festival (Mon – Wed).

Data: N/A

Earnings: N/A

Events: Market holidays in various APAC countries (e.g. China, Hong Kong, Japan etc.) on account of Mid-Autumn Festival (Mon – Wed); speech by the RBA’s Jones on at the Intersekt Festival (12:20am).

Data: Japanese imports/exports & trade balance (Aug, 12:50am); Japanese machinery tool orders (Jul, 12:50am); Australian Westpac leading index (Aug, 1:30am).

Earnings: N/A

Events: N/A

Data: Australian employment data (Aug, 2:30am).

Earnings: N/A

Events: PBoC (1 & 5 year LPR) policy decision (2am); BOJ policy decision.

Data: Japanese headline & core CPI (Aug, 12:30am).

Earnings: N/A

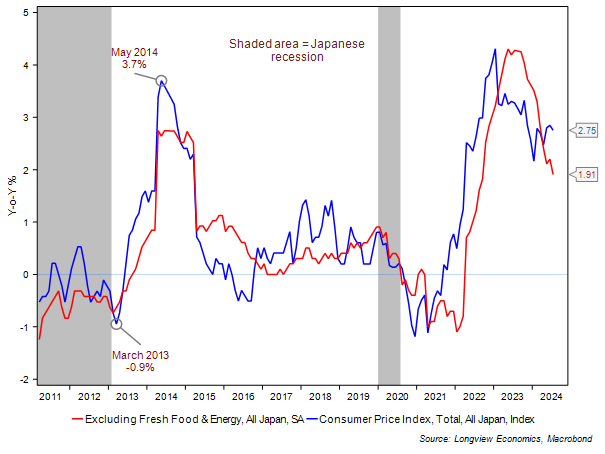

Fig E: Japanese headline & core CPI (Y-o-Y %)

Longview on Friday, 13th September 2024:

“How Strong is the US Consumer”

Quarterly Asset Allocation No. 59, 12th September 2024:

“China: Turning Japanese”

The SHORT VIEW (& market positioning), 10th September 2024:

“OIL: BUY Case Brewing”

Longview on Friday, 6th September 2024:

“Is This Time Different?”

Quarterly Asset Allocation No. 59, 5th September 2024:

“Eurozone: North – South Divide a.k.a. German Recession (likely) Coming”

Tactical Equity Asset Allocation No. 248, 5th September 2024:

“More (Wave 3) SELLing Expected a.k.a. Stay Tactically Cautious”

Monthly Global Asset Allocation No. 49, 3rd September 2024:

“Move NEUTRAL US Treasuries in Strategic Portfolio”