The State of Markets

The State of Markets

A brief review of all key upcoming events across the major regions of the globe & an overview of key recent market trends.

The State of Markets:

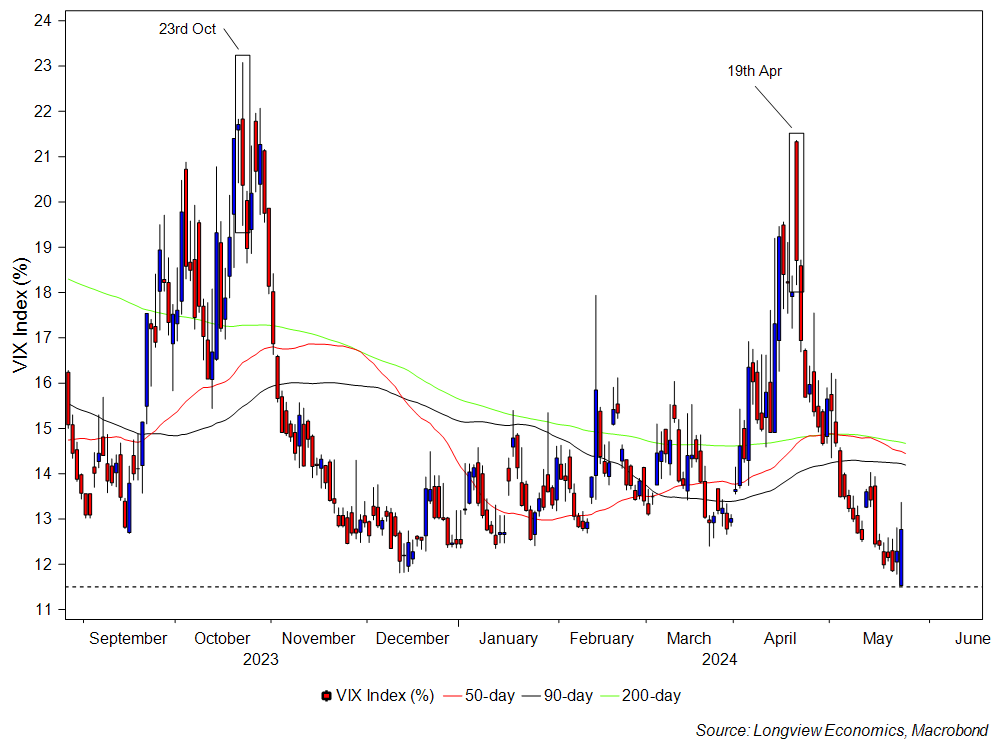

Equity markets have become complacently priced in recent weeks. In particular, as US equities have rallied back to their early April highs, volatility has fallen sharply (e.g. see the VIX’s new multi-year low last week –> chart below), downside put protection has been removed from portfolios, traded volumes have been low (indicative of low conviction in the rally), and risk appetite readings have become elevated (i.e. greedy).

That strength in equities has been somewhat driven by better than expected earnings results (with S&P500 companies beating estimates by 8.3% in aggregate, vs. the usual positive surprise of ~4%). US inflation has also been better than expected (and, linked to that, the dollar/bond yields have worked their way lower). In the near term, therefore, with plenty of good (earnings) news in the price, and given high levels of complacency, the question is: Are US equities now vulnerable to the downside? Or, with some indices breaking above their April highs this week, is upside momentum ongoing?

Our latest views, as always, are laid out in our key publications, including: i) ‘The Daily RAG Trader’ (1 – 2 weeks views on S&P500 futures); ii) ‘Tactical Asset Allocation’ (1 – 4 month views on the direction of global equity markets); & iii) our ‘Global Asset Allocation’ publication (with a 6 month to 2 year timeframe across all asset classes).

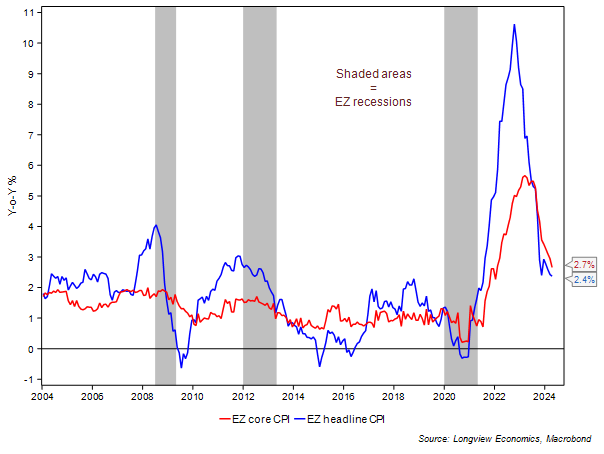

Next week’s macro data and earnings reports will be watched closely for further clues. In particular, there are several speeches by key FOMC members, including Mester, Kashkari, and Williams. Key US macro data includes house prices and pending home sales (Tuesday and Thursday), as well as PCE inflation data for April (Friday). Elsewhere German headline CPI is due on Wednesday, with Eurozone inflation on Friday. Please see below for a full list of key data and events.

Fig A: VIX candlestick chart shown with key moving averages (%)

(All in London time BST)

Events: Market holidays in the US on account of Memorial Day & the UK on account of Bank Holiday.

Data: German IFO business climate (May, 9am).

Earnings: N/A

Events: N/A

Data: US Conference Board consumer confidence (May, 3pm).

Earnings: N/A

Events: Fed releases Beige Book (7pm).

Data: Eurozone M3 money supply (Apr, 9am); German headline CPI (May first estimate, 1pm).

Earnings: Salesforce

Events: Speech by NY Fed’s Williams at Economic Club of New York (5:05pm).

Data: Eurozone unemployment rate (Apr, 10am).

Earnings: Costco.

Events: N/A

Data: Eurozone headline & core CPI (May first estimate, 10am); US personal income & spending including headline & core PCE inflation (Apr, 1:30pm); US Chicago PMI (May, 2:45pm).

Earnings: N/A

Global Macro Report, 22nd May 2024:

“How High is US Recession Risk? Is Growth Slowing? Have the US & EU Decoupled?”

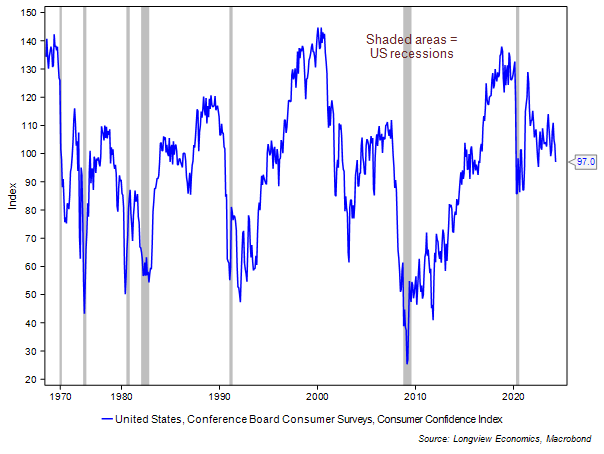

With the recent sharp fall in the US Citibank economic surprise index (fig 1), questions are being raised about the real strength of US economic growth. Q1 GDP data disappointed, coming in at 1.6% (vs. consensus of 2.5%); the ISM services index moved below 50; the combined ISM manufacturing and services employment sub-indices moved further below 50 (fig 14 in appendix); while the Michigan consumer ‘expectations less current situation’ model continues to signal recession (fig 2). Added to which, the yield curve remains inverted (22 months after its initial inversion), credit growth is anaemic and monetary policy appears tight.

Events: Market holiday in the US on account of Memorial Day.

Data: N/A

Earnings: N/A

Events: Speeches by the Fed’s Mester at Bank of Japan event (5:55am), Kashkari in London (2:55pm) and Cook on AI (6:05pm).

Data: US FHFA house price index (Mar, 2pm); US S&P/Case-Shiller 20-city & national house prices (Mar, 2pm); US Conference Board consumer confidence (May, 3pm); US Dallas Fed manufacturing activity (May, 3:30pm).

Earnings: N/A

Events: Speech by the Fed’s Williams at watertown community services roundtable (6:45pm); Fed releases Beige Book (7pm).

Data: US Richmond Fed manufacturing & business conditions (May, 3pm); US Dallas Fed services activity (May, 3:30pm).

Earnings: Salesforce, Agilent Technologies, HP

Events: Speeches by the Fed’s Bostic on the Economy (12am), Williams at Economic Club of New York (5:05pm) and Loan in Q&A (10pm).

Data: US GDP (Q1 second estimate, 1:30pm); US pending home sales (Apr, 3pm).

Earnings: Costco, Marvell, Dollar General.

Events: N/A

Data: Canadian monthly GDP (Mar, 1:30pm); US personal income & spending including headline & core PCE inflation (Apr, 1:30pm); US Chicago PMI (May, 2:45pm).

Earnings: N/A

Events: Speeches by the ECB’s Vujcic in China (4:40am) and Lane on Inflation in the Euro zone (12pm).

Data: German IFO business climate (May, 9am).

Earnings: N/A

Events: Speeches by the ECB’s Schnabel on price dynamics and monetary policy challenges (5:55am) and Knot at Barclays-CEPR International Monetary Policy Forum 2024 (5:55am).

Data: German wholesale price index (Apr, 7am); ECB 1 & 3 year inflation expectations (Apr, 9am).

Earnings: N/A

Events: Speech by the ECB’s Villeroy at presentation of bank supervisor ACPR's annual report (8am).

Data: German GfK consumer confidence (Jun, 7am); French INSEE consumer confidence (May, 7am); Italian ISTAT consumer & manufacturing confidence (May, 9am); Eurozone M3 money supply (Apr, 9am); German headline CPI (May first estimate, 1pm).

Earnings: N/A

Events: N/A

Data: Italian unemployment rate (Apr, 9am); Eurozone consumer confidence (May final estimate, 10am); Eurozone unemployment rate (Apr, 10am); Italian PPI (Apr, 10am).

Earnings: N/A

Events: Speech by the ECB’s Vujcic on Croatia's Economic and Financial Prospects in the euro-zone (7am) & Vujcic on Trends in International Trade and Financial Flows (8:30am).

Data: French total payrolls (Q1, 6:30am); German retail sales (Apr, 7am); French GDP & consumer spending (Q1 final estimate, 7:45am); French headline CPI (May first estimate, 7:45am); French PPI (Apr, 7:45am); Italian GDP (Q1 final estimate, 9am); Eurozone headline & core CPI (May first estimate, 10am); Italian headline CPI (May first estimate, 10am).

Earnings: N/A

Events: Market holiday on account of Bank Holiday.

Data: N/A

Earnings: N/A

Events: Speech by the Bank of England’s Haskel on UK inflation now and in the 1970s and lessons learnt (6pm).

Data: BRC shop price index (May, 12:01am); CBI distributive trends survey (May, 11am).

Earnings: N/A

Events: N/A

Data: N/A

Earnings: N/A

Events: Speech by the Bank of England’s Breeden at LSE (5pm).

Data: N/A

Earnings: N/A

Events: N/A

Data: Lloyds business barometer (May, 12:01am); Nationwide house prices (May, 7am); net consumer credit, mortgage approvals & M4 money supply (Apr, 9:30am).

Earnings: N/A

Events: N/A

Data: Chinese industrial profits (Apr, 2:30am); Japanese ESRI leading index (March final estimate, 6am).

Earnings: N/A

Events: Speech by the BOJ’s Ueda & Uchida at the at the BOJ-IMES conference (1:05am & 3:05am)

Data: Japanese PPI services (Apr, 12:50am).

Earnings: N/A

Events: Speech by the BOJ’s Adachi in Kumamoto (2:30am); speech by the RBA’s Hunter in Fireside chat (11:50pm).

Data: Australian Westpac leading index (Apr, 1:30am); Australian headline CPI (Apr, 2:30am); Japanese ESRI consumer confidence (May, 6am).

Earnings: ANTA Sports Products

Events: N/A

Data: Australian building approvals (Apr, 2:30am).

Earnings: N/A

Events: N/A

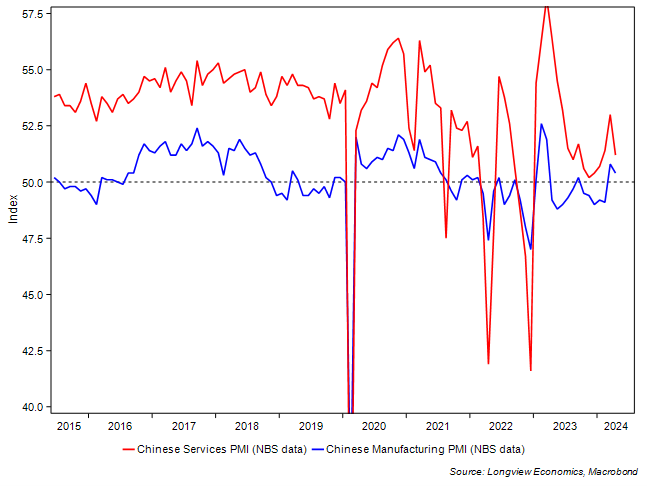

Data: Japanese jobless rate (Apr, 12:30am); Japanese retail sales & industrial production (Apr, 12:50am); Australian private sector credit (Apr, 2:30am); Chinese NBS manufacturing & service sector PMIs (May, 2:30am); Japanese housing starts (Apr, 6am).

Earnings: China Resources Land

Longview on Friday, 24th May 2024:

“The Big Issue”

Monthly Global Asset Allocation No. 40, 23rd May 2024:

“Keep Tilting Towards European Equities –> Theme is Evolving

A.k.a. Increase Italian, UK & Spanish OW Equity Positions”

Global Macro Report, 22nd May 2024:

“How High is US Recession Risk? Is Growth Slowing? Have the US & EU Decoupled?”

Longview on Friday, 17th May 2024:

“A New Cycle is Dawning – Part II”

Longview ‘Tactical’ Alert No. 81, 16th May 2024:

“Re-instate Tactical Equity Overweight Positions (for now)”

Monthly Global Asset Allocation No. 39, 15th May 2024:

“Chinese Equities: Move NEUTRAL (from OW) in Strategic Portfolio”

Commodity Fundamentals Report No. 183, 14th May 2024:

“Oil: Demand Drivers in 2024-25”