Tightening US Fiscal Policy – Implications Thereof

Tightening US Fiscal Policy – Implications Thereof

US Policy in 2023 -> Tight Monetary & Loose Fiscal

Over the course of the last 6 - 9 months, most investors (& Wall Street economists) have abandoned their recession calls from 20231, and switched to an expectation of a soft landing or indeed no landing at all. Despite various well regarded indicators forecasting a 2023 recession, it didn’t happen.

In line with that switch, the stock market has rallied, economic growth has remained robust (since then) and the labour market has appeared (at least on the surface) to remain strong (with ongoing robust non-farm payrolls2 and low weekly jobless claims).

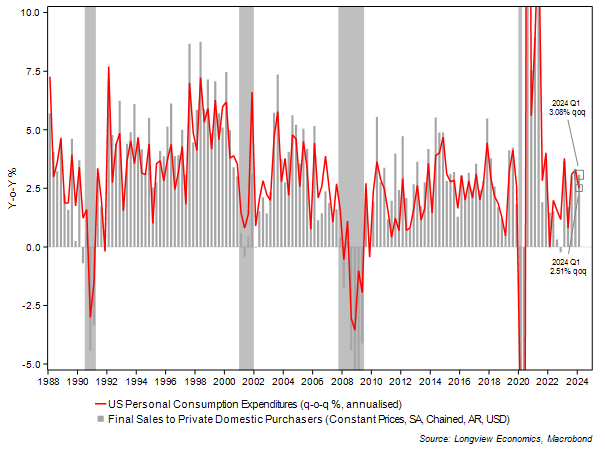

Confirming that, and despite a disappointing headline US Q1 GDP number, the underlying growth of the US economy has been resilient. Final sales to private domestic purchasers (a measure of underlying GDP, which strips out the volatile effects of inventories, exports and government spending) for example, grew by 3.1% in Q1 - one of its best growth rates in recent years. Personal consumption expenditure has also continued to grow at a solid pace (2.5% in q1 – fig 1).

In contrast, and as highlighted two weeks ago (HERE), growth in Europe and the UK has stagnated (i.e. flat lined for the past 1 – 2 years).

Fig 1: US GDP growth - underlying trends/components (q-o-q annualised %)

Differing fiscal policy has been one of the key drivers of those divergent growth outcomes (of the US and Europe/UK over the past 12 – 24 months).

The US, under the Biden Administration, has enacted three major fiscal stimulus programs (post pandemic) – the Infrastructure Act, CHIPS Act and the IRA (Inflation Reduction Act). All told, they have delivered major amounts of stimulus to the US economy. Some of it has been evident in the widening fiscal deficit in 2023 – other parts, though (including ‘CHIPs’ and ‘Infrastructure’ Acts loans and grants to the business sector), have been driving high business investment and rapid growth in non-residential construction spending (e.g. as new chips factories are built etc) – see below.

Other factors have also contributed to the economic growth gap, including the surge in US investment spending on AI (not matched elsewhere) and the larger stimulus during the pandemic (and therefore larger excess household savings in the US post pandemic, which underpinned growth in 2023).

So, while the EU has had some ongoing fiscal stimulus (the ‘NextGen EU’ support package), the numbers are much less dramatic and its fiscal consolidation has continued since 2020 (fig 10 in appendix).

In summary, therefore, the US economy experienced tight monetary policy in 2023 (as evidenced, for example, by no credit growth and minimal housing activity) but loose fiscal policy. In contrast, the UK & EZ had both tight fiscal and tight monetary policy last year (with that continuing so far in 2024).

US in 2024 -> Tight Monetary & Tightening Fiscal Policy

In 2024, though, the US situation is changing.

Keep reading with a 7-day free trial

Subscribe to The (Long)View From London to keep reading this post and get 7 days of free access to the full post archives.