The State of Markets

The State of Markets

A brief review of all key upcoming events across the major regions of the globe & an overview of key recent market trends.

The State of Markets: Wave Three Underway

US equity markets have continued to follow the classic ‘three wave’ sell-off pattern.

That is, the downtrend resumed last week (after a strong ‘wave 2’ relief rally in August). In particular, following a bearish key day reversal in late August (see chart below), the NASDAQ100 broke convincingly below its 50 day moving average on Wednesday and Thursday, before moving sharply lower yesterday (i.e. post the nonfarm payrolls report).

Risk aversion has also been building in other asset prices, many of which broke key levels last week. The US 10 year bond yield, for example, closed at new YTD lows yesterday (3.72%); oil broke below a multi-year support level (from last December); while the YEN, having strengthened in recent weeks, broke above its 5th August intraday highs yesterday.

The key question, therefore, is: What’s next? How much more downside is there in risk assets? And, with the NASDAQ100 testing its 200 day yesterday, has ‘wave 3’ finished? We outline our view on that in this week’s research, including in our Daily Risk Appetite publication, as well as in our Tactical Equity Asset Allocation research.

Next week’s macro data will be watched closely and includes the US CPI report (Wednesday); NFIB small business optimism (Tuesday); and Michigan sentiment (flash estimate for August, due on Friday). Key events include the first ‘Trump vs. Harris’ presidential debate on Tuesday and, in Europe, the ECB policy decision (Thursday). Please see below for a full list of key data and events next week.

Key chart: NASDAQ100 futures candlestick, shown with 50 & 200 day moving averages

(All in London time BST)

Events: N/A

Data: Chinese CPI & PPI (Aug, 2:30am); US consumer credit (Jul, 8pm).

Earnings: Oracle.

Events: Trump vs. Harris presidential debate (9:00 pm EDT).

Data: UK employment, jobless claims & average weekly earnings (Juk/Aug, 7am); US NFIB small business optimism (Aug, 11am).

Earnings: N/A

Events: N/A

Data: US headline & core CPI (Aug, 1:30pm); Chinese total social financing, new yuan loans, and M0, M1 & M2 money supply (Aug, 9am).

Earnings: Inditex.

Events: ECB policy decision (1:15pm) followed by press conference hosted by Lagarde (1:45pm).

Data: US headline & core PPI (Aug, 1:30pm).

Earnings: Adobe, Kroger.

Events: N/A

Data: US Michigan sentiment (September first estimate, 3pm).

Earnings: N/A

Monthly Global Asset Allocation No. 49, 3rd September 2024:

“Move NEUTRAL US Treasuries in Strategic Portfolio”

Consensus thinking in markets has changed rapidly in the past few months.

In April the market was concerned about sticky inflation, global growth expectations had risen to a two year high (according to the BAML survey); and many doubted that the Fed would cut rates in 2024. By late April, therefore, the 10 year yield had made a major (multi-month) high at 4.70%, while the rates market had largely priced out the chance of Fed cuts for the year.

Events: N/A

Data: US wholesale inventories (July final estimate, 3pm); US New York 1 year inflation expectations (Aug, 4pm); US consumer credit (Jul, 8pm).

Earnings: Oracle.

Events: Trump vs. Harris presidential debate (9:00 pm EDT).

Data: US NFIB small business optimism (Aug, 11am).

Earnings: N/A

Events: N/A

Data: US headline & core CPI (Aug, 1:30pm).

Earnings: N/A

Events: N/A

Data: Canadian building permits (Jul, 1:30pm); US headline & core PPI (Aug, 1:30pm); US weekly jobless claims (1:30pm); US household change in net worth (Q2, 5pm); US monthly budget statement (Aug, 7pm).

Earnings: Adobe, Kroger.

Events: N/A

Data: US export & import price index (Aug, 1:30pm); Canadian capacity utilisation rate (Q2, 1:30pm); US Michigan sentiment (September first estimate, 3pm).

Earnings: N/A

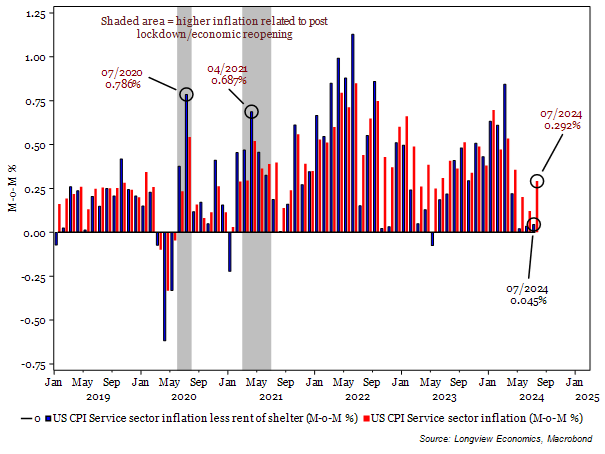

Fig B: US CPI Services and Services less rent of shelter (M-o-M %)

Events: N/A

Data: Eurozone Sentix investor confidence (Sep, 9:30am).

Earnings: N/A

Events: ISTAT publishes note on the Italian Economy (10am).

Data: German headline CPI (August final estimate, 7am); Italian industrial production (Jul, 9am).

Earnings: N/A

Events: N/A

Data: N/A

Earnings: Inditex.

Events: ECB policy decision (1:15pm) followed by press conference hosted by Lagarde (1:45pm).

Data: Italian unemployment rate (Q2, 9am).

Earnings: N/A

Events: Speech by the ECB's Rehn in Helsinki (9:30am).

Data: French headline & core CPI (August final estimate, 7:45am); French wages (Q2 final estimate, 7:45am); Eurozone industrial production (Jul, 10am).

Earnings: N/A

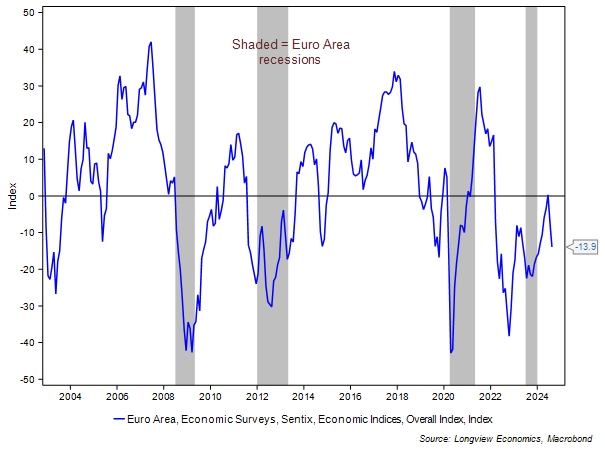

Fig C: Eurozone Sentix investor confidence (index)

Events: N/A

Data: N/A

Earnings: N/A

Events: N/A

Data: Employment, jobless claims & average weekly earnings (Jul/Aug, 7am).

Earnings: N/A

Events: N/A

Data: Monthly GDP estimate, industrial & manufacturing production, goods trade balance & construction output (July, 7am).

Earnings: N/A

Events: N/A

Data: RICS house price balance (Aug, 12:01am).

Earnings: N/A

Events: Bank of England releases inflation attitudes survey (9:30am).

Data: N/A

Earnings: N/A

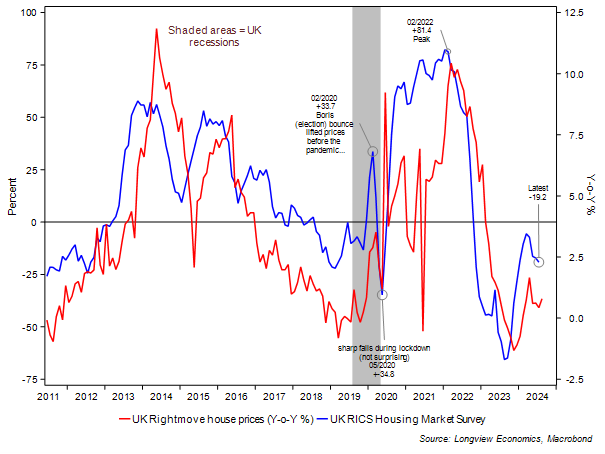

Fig D: UK RICS house price balance (index) against Rightmove house prices (Y-o-Y %)

Events: N/A

Data: Japanese GDP & bank lending (Q2 final estimate, 12:50am); Chinese CPI & PPI (Aug, 2:30am).

Earnings: N/A

Events: N/A

Data: Japanese M2 & M3 money supply (Aug, 12:50am); Australian Westpac consumer confidence (Sep, 1:30am); Australian NAB business confidence (Aug, 2:30am); Japanese machine tool orders (August first estimate, 7am).

Earnings: N/A

Events: Speech by the RBA's Hunter at the Barrenjoey Economic Forum (1:20am); speech by the BOJ's Nakagawa in Akita (2:30am).

Data: Chinese total social financing, new yuan loans, and M0, M1 & M2 money supply (Aug, 9am).

Earnings: N/A

Events: Speech by the BOJ’s Tamura in Okayama (2am).

Data: Japanese PPI (Aug, 12:50am); Australian consumer inflation expectation (Sep, 2am).

Earnings: N/A

Events: N/A

Data: Japanese industrial production & capacity utilisation (July final estimate, 5:30am).

Earnings: N/A

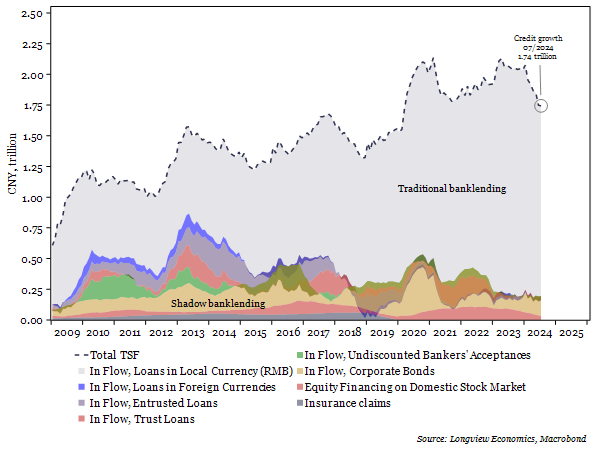

Fig E: Chinese total social financing (CNY, trillions)

Longview on Friday, 6th September 2024:

“Is This Time Different?”

Quarterly Asset Allocation No. 59, 5th September 2024:

“Eurozone: North – South Divide a.k.a. German Recession (likely) Coming”

Tactical Equity Asset Allocation No. 248, 5th September 2024:

“More (Wave 3) SELLing Expected a.k.a. Stay Tactically Cautious”

Monthly Global Asset Allocation No. 49, 3rd September 2024:

“Move NEUTRAL US Treasuries in Strategic Portfolio”

Longview on Friday, 30th August 2024:

“US Macro: Soft Landing or Recession?”

Global Macro Report, 29th August 2024:

“(State Based) Sahm Rule is Improving! A.k.a. Labour market not recessionary”

Monthly Global AA No. 48, 28th August 2024:

“Gold: Bull Run Ending? A.k.a. Reduce Weightings in the Strategic Portfolio”