The State of Markets

The State of Markets

A brief review of all key upcoming events across the major regions of the globe & an overview of key recent market trends.

The State of Markets:

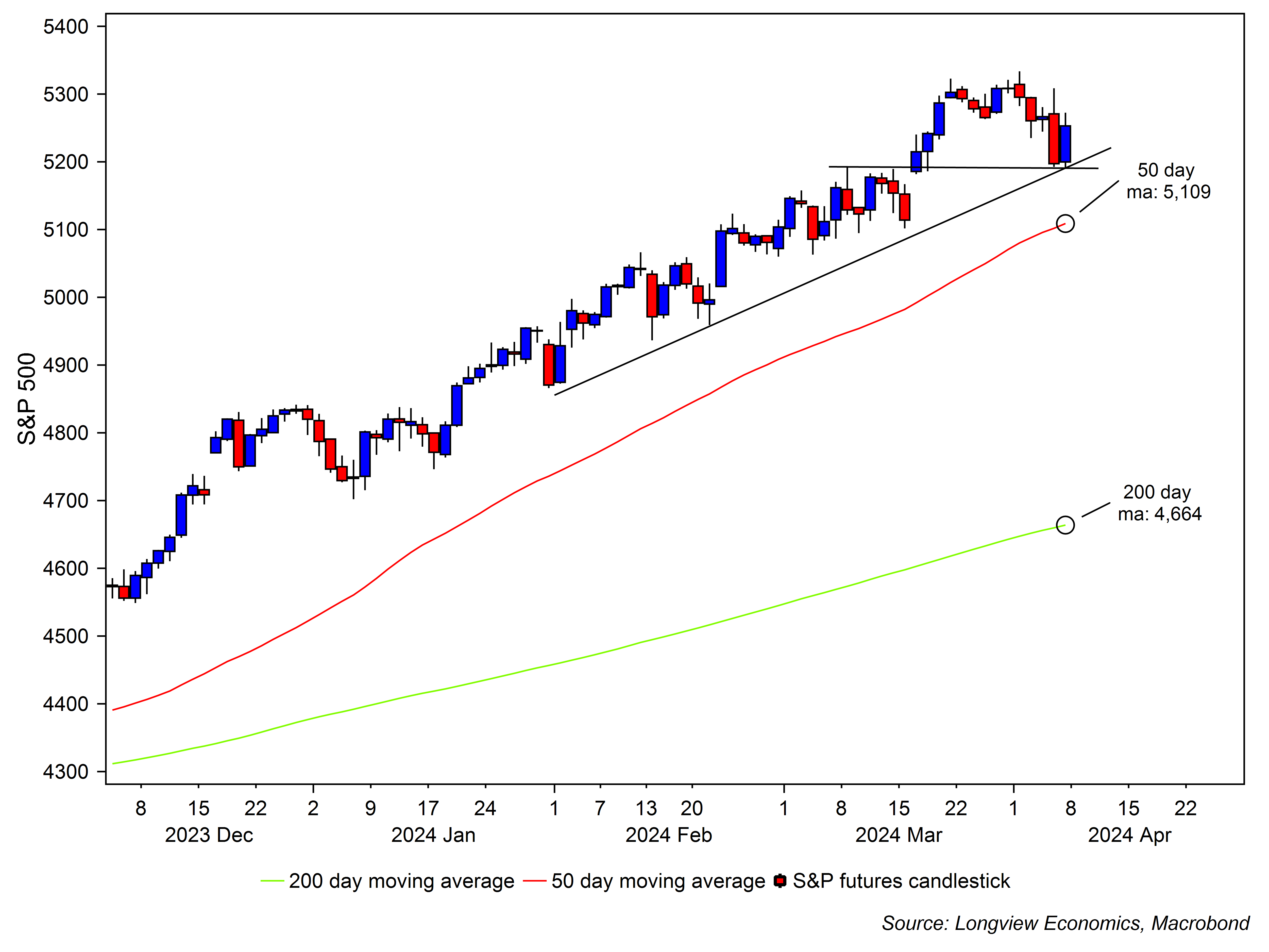

A bout of volatility returned to US equity markets last week. That seemed to be driven by rising geopolitical risks (and a higher oil price) on Thursday. Elsewhere the commentary from various Fed speakers was hawkish throughout the week and, on yesterday’s stronger than expected payrolls, there was further intra-day volatility in US equities (accompanied by higher bond yields and a stronger US dollar).

Broadly speaking, though, the S&P500 held above (and rallied from) key support levels. Those levels are shown in the chart below, and include the intra-day highs from early March, as well as the bottom of the recent uptrend channel. As such, while last week was testing for the bulls, the uptrend in the index remains intact (i.e. from that price action perspective).

The key question, therefore, is: Was higher volatility merely a ‘flash in the pan’, within an ongoing uptrend? Or was it the start of something more sinister?

While geopolitical risks bear watching closely, in that respect, next Wednesday’s US CPI report has the potential to drive the direction of the dollar, bond yields, and US/global equities. Other key data points include the NFIB small business optimism release (due Tuesday). Elsewhere, Chinese credit and money supply data is due on Friday. There’s also an ECB policy decision (and press conference) on Thursday. Please see below for a full list of next week’s key data/events.

Fig A: S&P500 futures candlestick with 50 & 200 day moving averages

(All in London time BST)

Events: N/A

Data: N/A

Earnings: N/A

Events: N/A

Data: Japanese machine tool orders (March first estimate, 7am); US NFIB small business optimism (Mar, 11am).

Earnings: N/A

Events: N/A

Data: US headline & core CPI (Mar, 1:30pm).

Earnings: Delta Air Lines.

Events: ECB policy decision (1:15pm) followed by a press conference hosted by Lagarde (1:45pm).

Data: Chinese PPI & CPI (Mar, 2:30am); Chinese total social financing, new yuan loans, and M0, M1 & M2 money supply – (Mar, time tentative).

Earnings: BlackRock.

Events: N/A

Data: N/A

Earnings: JPMorgan, Wells Fargo, Citigroup.

Extract from Commodity Fundamentals Report No. 179, 4th April 2024:

"OIL: SELL Case Brewing"

With oil prices up 25% since the December low, the consensus thinking in oil markets has become increasingly bullish.

There have been, of course, plenty of good reasons for a bullish view. US shale production growth, for example, has been slowing; OPEC+ has cut production in each of the past four months; while Chinese (& global) manufacturing activity has started to reaccelerate. Those bullish factors are laid out in detail HERE (as strong reasons to be positive on the oil price in recent months).

Those factors, though, appear to be largely priced in (at least for now). In December last year, the oil futures curve was nearly in contango (pricing excess supply in the global market). It’s now deeply backwardated (pricing in a tight supply and demand balance, see fig 7). That ‘tight pricing’ is mirrored, anecdotally, by the recent drumbeat of bullish commentary in the media (and calls for yet higher oil prices – see quotes above).

Events: Speech by the Fed's Kashkari in a townhall meeting at University of Montana (12:01am).

Data: US New York Fed 1 year inflation expectations (Mar, 4pm).

Earnings: N/A

Events: N/A

Data: US NFIB small business optimism (Mar, 11am).

Earnings: N/A

Events: Bank of Canada policy decision (2:45pm); speech by the Fed’s Goolsbee in a panel discussion (5:45pm); Fed's FOMC meeting minutes (7pm).

Data: Weekly MBA mortgage applications (12pm); Canada building permits (1:30pm); US headline & core CPI (Mar, 1:30pm); US wholesale inventories (Feb, 3pm); US monthly budget statement (Mar, 7pm).

Earnings: Delta Air Lines

Events: Fed's Williams gives keynote remarks (1:45pm); speech by the Fed’s Collins at the Economic Club of New York (5pm).

Data: US headline & core PPI (Mar, 1:30pm); US weekly jobless claims (1:30pm).

Earnings: BlackRock, Constellation Brands, Fastenal

Events: Speech by the Fed’s Daly in a Fireside chat (8:30pm).

Data: US trade balance (Mar, 1:30pm); Canada existing home sales (Mar, 2pm); US Michigan sentiment (April first estimate, 3pm).

Earnings: JPMorgan, Wells Fargo, Citigroup

Events: N/A

Data: German industrial production, trade balance, imports & exports (Feb, 7am); Eurozone Sentix investor confidence (Apr, 9:30am).

Earnings: Industrivarden

Events: ECB bank lending survey (9am).

Data: French trade balance (Feb, 7:45am).

Earnings: N/A

Events: N/A

Data: Italian retail sales (Feb, 9am).

Earnings: N/A

Events: ECB policy decision (1:15pm) followed by a ECB press conference hosted by Lagarde (1:45pm).

Data: Italian industrial production (Feb, 9am); German current account balance (Feb, 1:45am).

Earnings: N/A

Events: ECB survey of professional forecasters (9am).

Data: French headline & core CPI (March final estimate, 7:45am); Italian industrial sales (Jan, 9am).

Earnings: N/A

Events: Speech by BOE’s Breeden (4:30pm).

Data: N/A

Earnings: N/A

Events: N/A

Data: BRC retail sales (Mar, 12:01am).

Earnings: N/A

Events: N/A

Data: N/A

Earnings: N/A

Events: Speech by BOE’s Greene (7pm).

Data: RICS house price balance (Mar, 12:01am).

Earnings: N/A

Events: Bank of England releases Bernanke report on forecasting (12pm).

Data: Industrial & manufacturing production, goods trade balance, index of services & construction output (Feb, 7am).

Earnings: N/A

Events: N/A

Data: Japanese cash earnings (Feb, 12:30am); Japanese BoP trade balance (Feb, 12:50am); Australian home loans value (Feb, 2:30am).

Earnings: N/A

Events: N/A

Data: Australian Westpac consumer confidence (Apr, 1:30am); Australian NAB business confidence 2:30am); Japanese ESRI consumer confidence (Mar, 5am); Japanese machine tool orders (March first estimate, 7am).

Earnings: N/A

Events: N/A

Data: Japanese PPI & bank lending (Mar, 12:50am).

Earnings: Seven & I Holdings.

Events: N/A

Data: Japanese M2 & M3 money supply (Mar, 12:50am); Australian consumer inflation expectation (Apr, 2am); Chinese PPI & CPI (Mar, 2:30am); Chinese total social financing, new yuan loans, and M0, M1 & M2 money supply – (Mar, time tentative).

Earnings: Fast Retailing.

Events: N/A

Data: Chinese imports & exports (Mar, 4am).

Earnings: N/A

Longview on Friday, 5th April 2024:

"US & European Inflation – What’s Next?"

Commodity Fundamentals Report No. 179, 4th April 2024:

"OIL: SELL Case Brewing"

Tactical Equity Asset Allocation No. 243, 3rd April 2024:

“Equity Uptrend Ongoing (for now)"

Extract from Commodity Fundamentals Report No. 178, 28th March 2024:

“Copper: Breakout Underway?”

Longview ‘Tactical’ Alert No. 79, 26th March 2024:

“S&P500: 2013/17 – All over again? a.k.a. Should we expect summer volatility?”