The State of Markets

The State of Markets

A brief review of all key upcoming events across the major regions of the globe & an overview of key recent market trends.

The State of Markets:

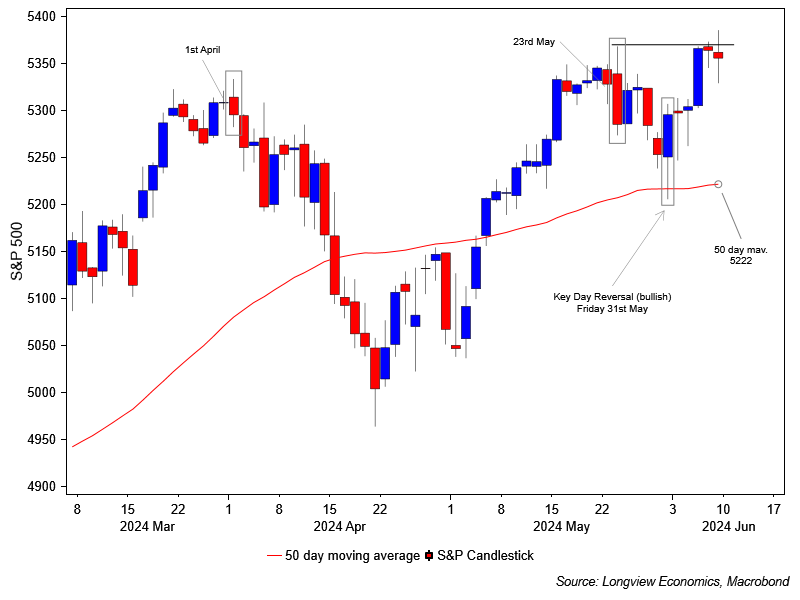

After posting a bullish key day reversal* pattern on Friday 31st May (10 days ago –> a positive ‘technical’ signal), the S&P500 rallied 1.3% last week and made another new record high. That strength was led by the tech sector and, specifically, the mega cap stocks. Nvidia, for example, was over 10% higher on the week; Amazon was 4.4% higher; while Microsoft was up over 2%. For most of the week, the rally was supported by the fall in bond yields & rate expectations (on weaker than expected ISM Manufacturing and ADP readings). On Friday, though, that reversed as nonfarm payrolls and wage inflation both surprised to the upside and yields backed up. Equites, though, remained relatively resilient.

The key question, therefore, is whether that resilience will persist in coming weeks? Our short-term view on equity market direction, as always, is laid out in our ‘Daily Risk Appetite Gauge’ publication (with ‘1 – 2’ week recommendations on S&P500 futures). Our medium term (‘1 – 4’ month view) is addressed in our monthly ‘Tactical Asset Allocation’ publication. This was updated last week – see below for detail. Longer term investors should refer to the ‘Strategic Global Asset Allocation’ reports (for our ‘6 months to 2 years’ recommended global asset allocation portfolio).

Next week is another big week for macro data and events, mostly notably with Wednesday’s US inflation report, which is then followed by the Fed’s policy decision, update of its economic projections (including the infamous ‘Dot Plots’) and press conference later that day (7pm & 7:30pm London time). Elsewhere NFIB small business optimism is due on Tuesday, with PPI (Thursday) and Michigan sentiment (Friday) both released later in the week. Outside the US, Chinese CPI is out on Wednesday and the BoJ will announce its policy decision on Friday. See below for a full list of key data/events.

Fig A: S&P500 futures candlestick shown with its 50-day moving average

(All in London time BST)

Events: N/A

Data: N/A

Earnings: N/A

Events: N/A

Data: UK unemployment, jobless claims & average earnings (Apr, 7am); US NFIB small business optimism (May, 11am).

Earnings: Oracle

Events: Fed policy decision (7pm) followed by Powell press conference & summary of economic projections (7:30pm).

Data: Chinese headline CPI & PPI (May, 2:30am); US headline & core CPI (May, 1:30pm).

Earnings: Broadcom

Events: N/A

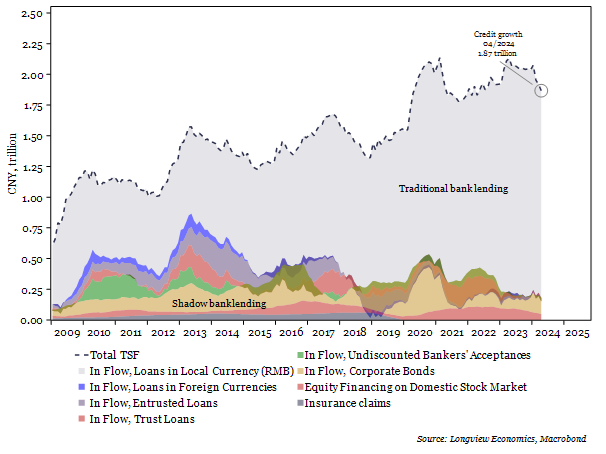

Data: UK RICS house price balance (May, 12:01am); Chinese total social financing, new yuan loans, and M0, M1 & M2 money supply (May, 9am).

Earnings: Adobe, Kroger

Events: BOJ policy decision.

Data: US Michigan sentiment (June first estimate, 3pm).

Earnings: N/A

Tactical Equity Asset Allocation No. 245, 6th June 2024:

““Upward Momentum Expected to Continue (for now)”

“The links are evident in history: Historical equity volatility has a 70%+ correlation with both implied volatility (i.e. as measured by the CBOE VIX index since 1990 and with corporate bond spreads – shown since 1928. Equity volatility and corporate bonds spreads are measures of the same thing - risk in the corporate sector. Both also have a strong relationship with the US corporate financing gap.”

Source: Longview Economics, August 2004, Structural Asset Allocation Research No. 5: “Equity Volatility: Low and set to stay low!”

So far in 2024, momentum in the US & global equity market has remained robust. The S&P500 is 12.5% higher; the NDX100 is up 13.1%, while various European indices have been equally strong (including Italy +14.4% and Spain +12.4%). A global equity index is up 10.3% (YTD). So, whilst the strongest major part of the global stock market has been the semiconductor stocks (Philly SOX +28%; Nvidia +147%), there’s been a broadening of participation in this rally in 2024 (versus the narrowness of the advance in most of 2023).

Events: N/A

Data: US New York Fed 1 year inflation expectations (May, 4pm).

Earnings: N/A

Events: N/A

Data: US NFIB small business optimism (May, 11am); Canadian building permits (Apr, 1:30pm).

Earnings: Oracle

Events: Fed policy decision & summary of economic projections (7pm) followed by Powell press conference (7:30pm).

Data: US headline & core CPI (May, 1:30pm); US monthly budget statement (May, 7pm).

Earnings: Broadcom.

Events: Fed’s Williams interviews Treasury Sec. Yellen (5pm).

Data: US weekly jobless claims (1:30pm); US headline & core PPI (May, 1:30pm).

Earnings: Adobe, Kroger.

Events: Speech by the Fed’s Goolsbee in Fireside chat (7pm).

Data: US import & export price index (May, 1:30pm); US Michigan sentiment (June first estimate, 3pm).

Earnings: N/A

Events: Speech by the ECB’s Holzmann on the central bank of the future (12pm).

Data: Italian industrial production (Apr, 9am); Eurozone Sentix investor confidence (Jun, 9:30am).

Earnings: N/A

Events: Speech by the ECB’s Villeroy in Paris (8:10am), Rehn in Helsinki (9am), Holzmann & Villeroy in Vienna (12pm), Lane in Dublin (12:05pm).

Data: N/A

Earnings: N/A

Events: Speech by the ECB’s Guindos at MNI Connect event (2pm).

Data: German headline CPI (May final estimate, 7am).

Earnings: N/A

Events: N/A

Data: German wholesale price index (May, 7am); Italian unemployment rate (Q1, 9am); Eurozone industrial production (Apr, 10am).

Earnings: N/A

Events: ECB’s Vasle addresses Slovenian bankers (8:35am), Lane & Lagarde on panel at 30th Dubrovnik Economic conference (10am & 6:30pm).

Data: French headline & core CPI (May final estimate, 7:45am); French wages (Q1 final estimate, 7:45am); Eurozone trade balance (Apr, 10am).

Earnings: N/A

Events: N/A

Data: N/A

Earnings: N/A

Events: N/A

Data: Employment, jobless claims & average weekly earnings (Apr, 7am).

Earnings: N/A

Events: N/A

Data: Monthly GDP estimate, industrial & manufacturing production, goods trade balance & construction output (Apr, 7am).

Earnings: N/A

Events: N/A

Data: RICS house price balance (May, 12:01am).

Earnings: N/A

Events: Bank of England releases inflation attitudes survey (9:30am).

Data: N/A

Earnings: N/A

Events: Market holiday in China & Hong Kong on account of Dragon Boat Festival & in Australia on account of King’s Birthday (Mon).

Data: Japanese GDP (Q1 final estimate, 12:50am); Japanese bank lending (May, 12:50am).

Earnings: N/A

Events: N/A

Data: Japanese M2 & M3 money supply (May, 12:50am); Australian NAB business confidence (May, 2:30am); Japanese machine tool orders (May first estimate, 7am).

Earnings: N/A

Events: N/A

Data: Japanese PPI (May, 12:50am); Chinese headline CPI & PPI (May, 2:30am).

Earnings: N/A

Events: N/A

Data: Australian CBA household spending (May, 12am); Australian employment data (May, 2:30am); Chinese total social financing, new yuan loans, and M0, M1 & M2 money supply (May, 9am).

Earnings: N/A

Events: BOJ policy decision (Fri).

Data: Japanese industrial production & capacity utilisation (April final estimate, 5:30am).

Earnings: N/A

Longview on Friday, 7th June 2024:

“Small - Not So Beautiful (Yet)…”

Tactical Equity Asset Allocation No. 245, 6th June 2024:

“Upward Momentum Expected to Continue (for now)”

Quarterly Asset Allocation No. 58, 4th June 2024:

“Eurozone: Above Trend Growth Ahead”

Longview on Friday, 31st May 2024:

“Large Cap Stock Bubble (Tech & non-Tech)”

Quant Monthly Appendices 1 & 2, 30th May 2024:

“Country & S&P500 Sector Valuation Overview”

Global Macro Report, 29th May 2024:

“Japanese CPI: 'Hot or Not'? a.k.a. Is Japan emerging from its long slumber?”