The State of Markets

A brief review of all key upcoming events across the major regions of the globe & an overview of key recent market trends.

The State of Markets: “The January Effect”

After an unusually weak December (S&P500 was -2.5%), without its typical Santa Claus rally, the debate continues as to how will the US (& other) equity markets perform in 2025. Most Wall Street strategists are bullish for the year.

We outlined our short term (1 – 4 month) views on US equity markets in our latest ‘Tactical Equity Asset Allocation’ publication (available to ‘Tactical’ subscribers, published in early December & titled: “This Bull Run (since Oct ’22) is Tired!, A.k.a. But Stay Tactically OW (for now)”); as well as our longer-term views (i.e. 6 months to 2 years) in our latest ‘Strategic Global Asset Allocation’ publication (published just prior to Christmas – see snippet below).

Elsewhere the January effect is often watched closely to give clues as to the outlook for the year. There’s a view in markets that “how goes January, so goes the year”. Those relationships, however, are weak. Our analysis of the correlation of the performance of both the first trading day and the first week of January with the year found, in both instances, only a trivial R squared (of 0.01 and 0.001). That is, there’s no clear evidence for the ‘January effect’ over the 85 years of data that we examined (1929 – 2014).

Next week brings the first full trading week of the year. The key data comes out at the end of the week with the US monthly non-farm payrolls, average hourly earnings and unemployment rate released on Friday. Ahead of that, ISM services data is released on Tuesday; with various other labour market data coming out over the course of the week (including JOLTS on Tuesday; ADP on Wednesday; & Challenger job cuts on Thursday). It’s also a key week for inflation data (EZ CPI is on Tuesday; Chinese CPI and PPI are on Thursday). A full list of key events next week is laid out below.

(All in London time BST)

Events: N/A

Data: Chinese Caixin service sector PMI (Dec, 1:45am); German headline CPI (December first estimate, 1pm).

Earnings: N/A

Events: N/A

Data: Eurozone headline & core CPI (December first estimate, 10am); US JOLTS job openings (Nov, 3pm); US ISM services (Dec, 3pm).

Earnings: N/A

Events: Fed minutes from December meeting (7pm).

Data: US ADP employment change (Dec, 1:15pm).

Earnings: N/A

Events: N/A

Data: Chinese headline CPI & PPI (Dec, 1:30am); US Challenger job cuts (Dec, 12:30pm).

Earnings: N/A

Events: N/A

Data: US nonfarm payrolls, hourly earnings & unemployment (Dec, 1:30pm); US Michigan Sentiment (January first estimate, 3pm); Chinese total social financing, new yuan loans, and M0, M1 & M2 money supply (Dec, time tentative).

Earnings: N/A

Quarterly Asset Allocation No. 60, 23rd December 2024:

“Risks Rising - (Start) Reducing Risk Exposure in Strategic Portfolio A.k.a. Stay OW (for now) BUT at Reduced Position Size”

Compelling opportunities in markets occur when there’s a strong consensus amongst investors (with crowded, one-way positioning) and there’s a good macro reason to face the other way (and bet against the crowd).

Next year, especially the first half of the year, is building towards one of those compelling opportunities. That is, this bull run in US large cap equities is looking increasingly tired and overextended, whilst the case for a US mid cycle economic slowdown is brewing. That combination of factors sets the stage for a meaningful pullback in global equity markets in the first half of 2025. For now, we are waiting for evidence of the final ‘blow off top’ phase before moving fully defensive in our portfolios. Given, rising risk levels, though, (and our heavily overweight recommended risk positioning), we advise reducing risk levels in the portfolio (albeit remaining ‘risk on’).

Events: Speech by the Fed’s Cook on the Economic outlook and financial stability (2:15pm).

Data: Canadian S&P service sector PMI (Dec, 2:30pm); US S&P service sector PMI (December final estimate, 2:45pm); US durable goods orders (November final estimate, 3pm).

Earnings: N/A

Events: The Fed’s Barkin speaks to Raleigh Chamber (1pm).

Data: US trade balance (Nov, 1:30pm); US JOLTS job openings (Nov, 3pm); US ISM services (Dec, 3pm).

Earnings: N/A

Events: Speech by the Fed’s Waller on the Economic outlook (1:30pm); Fed minutes from December meeting (7pm).

Data: US ADP employment change (Dec, 1:15pm); US consumer credit (Nov, 8pm).

Earnings: N/A

Events: Speeches by the Fed’s Harker on the Economic outlook (2pm), Barkin at the Virginia Bankers Association (5:40pm), Schmid at the Economic Club of Kansas City (6:30pm) & Bowman reflects on 2024 (6:35pm).

Data: NFIB small business optimism (Dec, 11am); US Challenger job cuts (Dec, 12:30pm); US weekly jobless claims (1:30pm); US wholesale inventories (November final estimate, 3pm).

Earnings: N/A

Events: N/A

Data: Canadian employment change (Dec, 1:30pm); US nonfarm payrolls, hourly earnings & unemployment (Dec, 1:30pm); Canadian building permits (Nov, 1:30pm); US Michigan Sentiment (January first estimate, 3pm).

Earnings: Constellation Brands, Delta Air Lines.

Events: N/A

Data: HCOB services sector PMIs for Spain (8:15am), Italy (8:45am), France (8:50am), Germany (8:55am) & Eurozone (9am) – all December final estimates apart from Spain & Italy; Eurozone Sentix investor confidence (Jan, 9:30am); German headline CPI (December first estimate, 1pm).

Earnings: N/A

Events: N/A

Data: French headline CPI (December first estimate, 7:45am); ECB 1 & 3 year inflation expectations (Nov, 9am); Italian unemployment rate (Nov, 9am); Eurozone headline & core CPI (December first estimate, 10am); Italian headline & core CPI (December first estimate, 10am); Eurozone unemployment rate (Nov, 10am).

Earnings: N/A

Events: Speech by the ECB’s Villeroy in Paris (Wed, 5:30pm).

Data: German retail sales (Nov, 7am); German factory orders (Nov, 7am); French INSEE consumer confidence (Dec, 7:45am); Eurozone consumer confidence (December final estimate, 10am); Eurozone PPI (Nov, 10m).

Earnings: N/A

Events: N/A

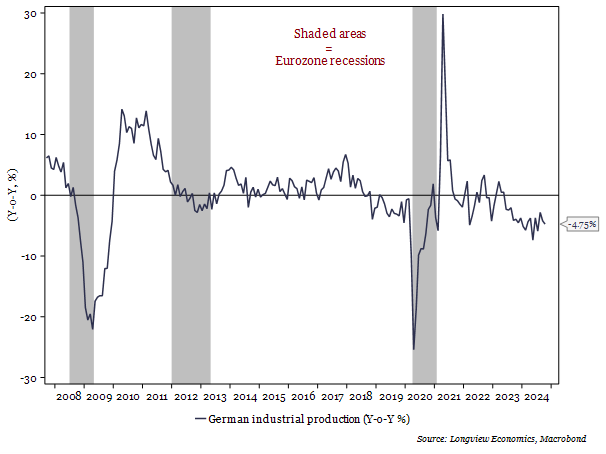

Data: German industrial production (Nov, 7am); German imports/exports, & trade balance (Nov, 7am); Eurozone retail sales (Nov, 10am).

Earnings: N/A

Events: N/A

Data: French consumer spending (Nov, 7:45am); French industrial & manufacturing production (Nov, 7:45am); Spanish industrial production (Nov, 8am); Italian retail sales (Nov, 9am).

Earnings: N/A

Events: N/A

Data: New car sales (Dec, 9am); S&P service sector PMI (December final estimate, 9:30am).

Earnings: N/A

Events: N/A

Data: BRC retail sales (Dec, 12:01am); Halifax house prices (Dec, 7am).

Earnings: N/A

Events: N/A

Data: N/A

Earnings: N/A

Events: Speech by the Bank of England’s Breeden at the University of Edinburgh (4pm).

Data: BRC shop price index (Dec, 12:01am).

Earnings: N/A

Events: N/A

Data: N/A

Earnings: N/A

Events: N/A

Data: Japanese Jibun Bank service sector PMI (December final estimate, 12:30am); Chinese Caixin service sector PMI (Dec, 1:45am); Japanese money supply (Dec, 11:50pm).

Earnings: N/A

Events: N/A

Data: Australian building approvals (Nov, 12:30am).

Earnings: N/A

Events: N/A

Data: Australian headline CPI (Nov, 12:30am); Australian job vacancies (Nov, 12:30am); Japanese ESRI consumer confidence (Dec, 5am); Japanese cash earnings (Nov, 11:30pm).

Earnings: N/A

Events: N/A

Data: Australian retail sales (Nov, 12:30am); Australian imports/exports, & trade balance (Nov, 12:30am); Chinese headline CPI & PPI (Dec, 1:30am); Japanese household spending (Nov, 11:30pm).

Earnings: N/A

Events: N/A

Data: Australian household spending (Nov, 12:30am); Japanese ESRI leading index (November first estimate, 5am); Chinese total social financing, new yuan loans, and M0, M1 & M2 money supply (Dec, time tentative).

Earnings: N/A

N/A

Quarterly Asset Allocation No. 60, 23rd December 2024:

“Risks Rising - (Start) Reducing Risk Exposure in Strategic Portfolio A.k.a. Stay OW (for now) BUT at Reduced Position Size”