The State of Markets

The State of Markets

A brief review of all key upcoming events across the major regions of the globe & an overview of key recent market trends.

The State of Markets:

Tech has been the driving force for US equities in recent months, particularly since late April. In the last two weeks, though, some cracks have started to emerge. In particular, following bearish key day reversals in the NDX100 and Philly SOX (20th June), upward momentum in the NDX100 has stalled while the Philly SOX closed down for the second week in a row. With that, key semiconductor stocks, including Broadcom (-12%) and Micron (-14%), have sold off sharply from their mid-June highs.

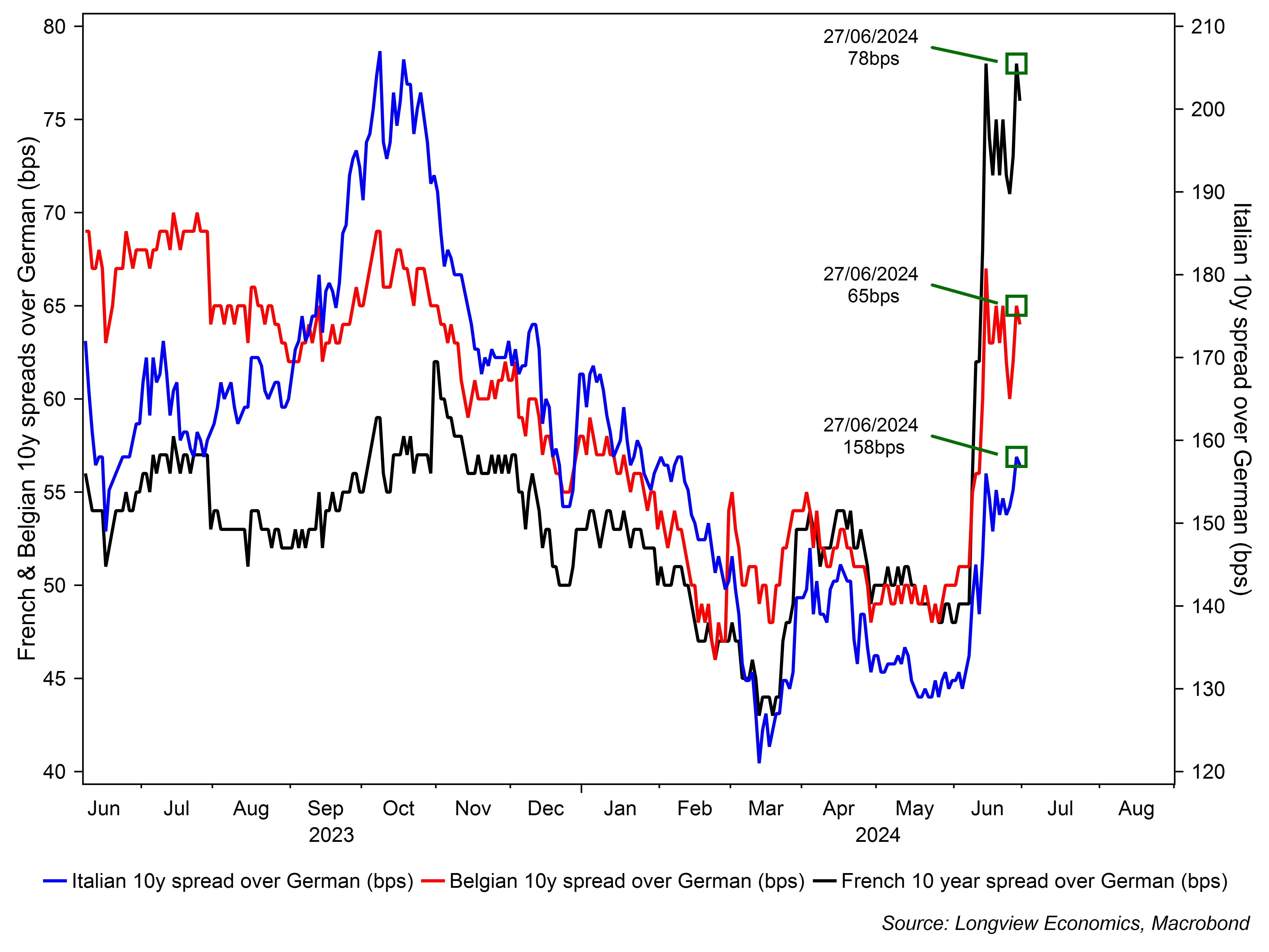

Elsewhere Eurozone sovereign spreads have been widening (see key chart below). Tomorrow is the first round of voting in the French elections, with far right groups leading in the polls. The key risk is that spreads widen further on the result, and generate more weakness in European equities. In that respect, a policy response from the ECB remains unlikely (for now – i.e. in the absence of wider spreads).

Several other key events will be watched closely by markets this coming week. Most notably US ISM manufacturing is due on Monday, followed by JOLTS job openings (Tuesday), ADP employment & ISM services (Wednesday), and nonfarm payrolls (on Friday). Elsewhere the minutes from the June Fed meeting will be released (Wednesday) and, in Europe, the first CPI estimate for June is due on Tuesday. Please see below for a full list of key data & events.

Fig A: French, Italian & Belgium spreads over 10 year bunds (bps)

(All in London time BST)

Events: First round result of French elections (Sunday/Monday); ECB forum on central banking in Sintra with speakers including Lagarde & Powell.

Data: Chinese Caixin manufacturing sector PMI (Jun, 2:45am); US ISM manufacturing (Jun, 3pm).

Earnings: N/A

Events: N/A

Data: Eurozone headline & core CPI (June first estimate, 10am); US JOLTS job openings (May, 3pm).

Earnings: N/A

Events: Fed minutes from June meeting (7pm), early close in the US.

Data: US ADP employment change (Jun, 1:15pm); US ISM services (Jun, 3pm).

Earnings: N/A

Events: ECB publishes account from June policy meeting (Thurs, 12:30pm) & bank holiday (on Thursday) on account of Independence Day (July 4th); UK General Election (Thursday – all day).

Data: German factory orders (May, 7am).

Earnings: N/A

Events: N/A

Data: US nonfarm payrolls, hourly earnings & unemployment (Jun, 1:30pm).

Earnings: N/A

Monthly Global Asset Allocation No. 41, 26th June 2024:

“Gold: Stay OW in Strategic Portfolio (for now) A.k.a. Risks Rising”

For most of the past 30 - 40 years, the US economy has been operating a debt financed monetary system. That is, phases of growth have been supported by growing indebtedness on sectoral balance sheets (somewhere). In the 1980s, it was the US & UK household balance sheets; in the 1990s, it was balance sheets in other parts of the world (South East Asian tigers, Russia, derivatives books of the major global banks etc); in the noughties, it was once again household and commercial bank balance sheets in the West (and parts of the Eurozone – e.g. Spain etc). This past 15 years, it’s been Western central bank & government balance sheets, whilst China has aggressively leveraged up across its entire economy.

Events: Bank holiday in Canada on account of Canada Day.

Data: US S&P manufacturing sector PMI (June final estimate, 2:45pm); US ISM manufacturing (Jun, 3pm) & construction spending (May, 3pm).

Earnings: N/A

Events: Chair Powell at ECB Sinatra Forum on Policy Panel (8:30am).

Data: Canadian S&P manufacturing PMI (Jun, 2:30pm); US JOLTS job openings (May, 3pm).

Earnings: N/A

Events: Speech by the Fed’s Williams at ECB forum (12pm) & Fed minutes from June meeting (7pm).

Data: US Challenger job cuts (Jun, 12:30pm); US ADP employment change (Jun, 1:15pm); US trade balance (May, 1:30pm); US weekly jobless claims (1:30pm); US S&P service sector PMI (June final estimate, 2:45pm); US durable goods orders (May final estimate, 3pm); US ISM services (Jun, 3pm).

Earnings: Constellation Brands.

Events: Bank holiday on account of Independence Day (July 4th).

Data: Canadian S&P service sector PMI (Jun, 2:30pm).

Earnings: N/A

Events: Williams again at an event organised by the Reserve Bank of India (10:40am).

Data: Canadian employment change (Jun, 1:30pm); US nonfarm payrolls, hourly earnings & unemployment (Jun, 1:30pm).

Earnings: N/A

Events: First round result of French elections (Sunday/Monday); speeches by the ECB’s Nagel (Mon, 1:15pm) & Lagarde in Sintra (Mon, 8pm).

Data: HCOB manufacturing sector PMIs for Italy (8:45am), France (8:50am), Germany (8:55am) & Eurozone (9am) – all final estimates apart from Italy; German headline CPI (June first estimate, 1pm); Italian new car sales (Jun, 5pm).

Earnings: N/A

Events: Guindos, Elderson, Schnabel, Lagarde in Sintra panel (8:30am – 2:30pm).

Data: Italian unemployment rate (May, 9am); Eurozone headline & core CPI (June first estimate, 10am); Eurozone unemployment rate (May, 10am).

Earnings: N/A

Events: Guindos, Cipollone, Lane, Knot & Lagarde in Sintra panel (9am – 3:15pm).

Data: HCOB service sector PMIs for Italy (8:45am), France (8:50am), Germany (8:55am) & Eurozone (9am) – all final estimates apart from Italy; Eurozone PPI (May, 10am).

Earnings: N/A

Events: ECB publishes account from June policy meeting (12:30pm).

Data: German factory orders (May, 7am).

Earnings: N/A

Events: Nagel on the digital euro and the protection of privacy (8am) & Lagarde in Aix (6:15pm).

Data: German industrial production (May, 7am); French industrial & manufacturing production (May, 7:45am); Italian retail sales (May, 9am); Eurozone retail sales (May, 10am).

Earnings: N/A

Events: N/A

Data: Nationwide house prices (Jun, 7am); net consumer credit, mortgage approvals & M4 money supply (May, 9:30am); S&P manufacturing sector PMI (June final estimate, 9:30am).

Earnings: N/A

Events: N/A

Data: BRC retail prices (Jun, 12:01am).

Earnings: Sainsbury’s.

Events: N/A

Data: S&P services & composite sector PMIs (June final estimate, 9:30am).

Earnings: N/A

Events: UK General Election (Thursday – all day).

Data: New car sales (Jun, 9am); S&P construction sector PMI (Jun, 9:30am).

Earnings: N/A

Events: N/A

Data: N/A

Earnings: N/A

Events: N/A

Data: Australian Judo Bank manufacturing sector PMI (June final estimate, 12am); Japanese Tankan manufacturing & service sector PMIs (Q2, 12:50am); Japanese Jibun Bank manufacturing sector PMI (June final estimate, 1:30am); Australian headline CPI (Jun, 2am); Australian ANZ-Indeed job advertisements (Jun, 2:30am); Chinese Caixin manufacturing sector PMI (Jun, 2:45am); Japanese ESRI consumer confidence (Jun, 6am).

Earnings: N/A

Events: RBA minutes from June policy meeting (2:30am).

Data: Japanese money supply (Jun, 12:50am).

Earnings: N/A

Events: N/A

Data: Australian Judo Bank service & composite sector PMI (June final estimate, 12am); Japanese Jibun Bank service & composite sector PMI (June final estimate, 1:30am); Australian building approvals, private sector houses & retail sales (May, 2:30am); Chinese Caixin service & composite sector PMI (Jun, 2:45am).

Earnings: N/A

Events: N/A

Data: Japanese household spending (May, 12:30am); Japanese ESRI leading index (May first estimate, 6am).

Earnings: N/A

Events: N/A

Data: N/A

Earnings: N/A

Longview on Friday, 28th June 2024:

“US Wealth Growing Across All Income Groups”

Quarterly Asset Allocation No. 58, 28th June 2024:

“Reduce Bond & Some EZ Equity Weightings (for now)”

Monthly Global Asset Allocation No. 41, 26th June 2024:

“Gold: Stay OW in Strategic Portfolio (for now) A.k.a. Risks Rising”

Global Macro Report, 25th June 2024:

“BoE Too Slow to Cut Rates A.k.a. Growing Risk of Oversteer”

Longview on Friday, 21st June 2024:

“Is a Currency Crisis (& Secular Dollar Bear Market) Brewing?”

Quarterly Asset Allocation No. 58, 20th June 2024:

“How Magnificent Are the ‘MAG7’?”

Quarterly Asset Allocation No. 58, 17th June 2024:

“US Expansion Likely Ongoing (Recession Risk = 20%)”