The State of Markets

The State of Markets

A brief review of all key upcoming events across the major regions of the globe & an overview of key recent market trends.

The State of Markets:

Nvidia and US government bonds have been two of the key features of markets this week (so far).

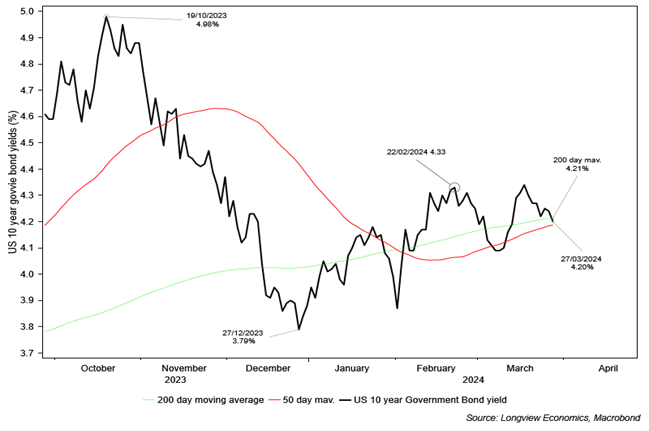

US 10-year bond yields have been trying (again) to break out of their range of recent weeks. That range, which has been in place since mid-February, is between 4.17% and 4.33% yield (except for a 5-day dip lower in yields in mid-March). As of Wednesday’s close, the yield was at the bottom end of that range and again below its 200-day moving average (with yields trading lower again, as at the time of writing on Thursday). Tomorrow’s PCE deflator data will be key, in that respect, given the current ‘sticky inflation’ debate (along with any comments from Powell).

Nvidia, meanwhile, has bucked the market trend this week. The S&P500 has (so far) traded broadly flat, whilst Nvidia is down 4% (as of Wednesday’s close). With that, it has failed to break technical resistance at its 8th March intraday highs (i.e. $973.8, currently trading at $907.7). As a key leadership stock this year, its recent underperformance likely points either to: i) a market pullback; or ii) a switch in leadership.

Next week is key for US data releases. Friday’s non-farm payrolls, ISM manufacturing and services surveys, as well as the JOLTS data are all published. The employment sub-indices of the ISM surveys, as well as the ‘household’ jobs survey will also all be watched closely. Those labour market data points have been considerably weaker than the ADP & NFP data. Equally job openings, quits and hires rates have all softened in recent months. By the end of next week, an updated picture of the labour market will have emerged.

For the full list of key events next week, by region, see below.

Fig A: US 10-year bond yields shown with key moving averages

(All in London time BST)

Events: N/A

Data: US ISM manufacturing (Mar, 3pm).

Earnings: N/A

Events: N/A

Data: UK net lending to individuals, consumer credit, mortgage approvals & M4 money supply (Feb, 9:30am); German headline & core CPI preliminary estimate (Mar, 1pm); US JOLTS job openings (Feb, 3pm).

Earnings: N/A

Events: Fed's Powell speaks at Stanford Event (5:10pm)

Data: Eurozone headline & core CPI flash estimate (Mar, 10am); US ADP employment change (Mar, 1:15pm); US ISM services (Mar, 3pm).

Earnings:

Events: N/A

Data: Eurozone core & headline PPI (Feb, 10am).

Earnings: N/A

Events: N/A

Data: US nonfarm payrolls, hourly earnings & unemployment data (Mar, 1:30pm).

Earnings: N/A

Extract from Commodity Fundamentals Report No. 178, 28th March 2024:

“Copper: Breakout Underway?”

From March 2022 through to July 2022, copper sold off sharply (down by 35%), as the Fed, and other central banks, raised interest rates and lockdowns in China became more draconian (most notably in Shanghai, from March/April onwards). Since that initial local low, the price then generated a series of ‘higher lows’ and ‘lower highs’, such that a ‘pennant formation’ (technical price pattern) was created (fig 1).

This past month, though, the copper price has rallied sharply and broken above the upper end of its pennant range (i.e. broken out of it). Typically, breakouts of pennant formations signal a key change in the price trend (in this case, potentially the start of a new bull run).

Events: N/A

Data: Canadian S&P manufacturing sector PMI (Mar, 2:30pm); US S&P manufacturing sector PMI (Mar, 2:45pm); US construction spending (Feb, 3pm); US ISM manufacturing (Mar, 3pm); Canadian BoC business outlook survey (Q1, 3:30pm).

Earnings: N/A

Events: Fed's Williams moderates discussion at Economic Club of NY (5pm); Fed's Mester gives remarks on economic outlook (5:05pm); Fed's Daly participates in fireside chat (6:30pm).

Data: US JOLTS job openings (Feb, 3pm); US factory orders (Feb, 3pm); US Wards total vehicle sales (Mar, 10pm).

Earnings: Paychex

Events: Fed's Goolsbee gives opening remarks at a Bank of Chicago virtual event (5pm); Fed's Powell speaks at Stanford Event (5:10pm).

Data: US weekly MBA mortgage applications (12pm); US ADP employment change (Mar, 1:15pm); Canadian S&P services sector PMI (Mar, 2:30pm); US S&P services sector PMI (Mar, 2:45pm); US ISM services (Mar, 3pm).

Earnings: N/A

Events: Fed's Harker participates in fireside chat (3pm); Fed's Goolsbee participates in a moderated Q&A (5:45pm); Fed's Mester gives remarks on economic outlook (7pm).

Data: US Challenger job cuts (Mar, 12:30pm); US trade balance, exports & imports (Feb, 1:30pm); US weekly jobless claims (1:30pm).

Earnings: N/A

Events: Fed's Musalem gives introductory remarks before the 2024 Women in Economics Symposium hosted by the Federal Reserve Bank of St. Louis (12:20am).

Data: Canadian unemployment rate (Mar, 1:30pm); US nonfarm payrolls, hourly earnings & unemployment data (Mar, 1:30pm); Canadian Ivey PMI (Mar, 3pm); US consumer credit (Feb, 8pm).

Earnings: N/A

Events: Market Holiday – Easter.

Data: N/A

Earnings: N/A

Events: N/A

Data: Italian manufacturing PMI (Mar, 8:45am); French manufacturing PMI (March final estimate, 8:50am); German manufacturing PMI (March final estimate, 8:55am); Eurozone manufacturing PMI (March final estimate, 9am); ECB 1 & 3 year inflation expectations (Feb, 9am); German headline & core CPI preliminary estimate (Mar, 1pm).

Earnings: N/A

Events: N/A

Data: Italian unemployment rate (Feb, 9am); Eurozone headline & core CPI flash estimate (Mar, 10am); Eurozone unemployment rate (Feb, 10am).

Earnings: N/A

Events: ECB Publishes Account of March Rate Decision (12:30pm).

Data: Italian services PMI (Mar, 8:45am); French services PMI (March final estimate, 8:50am); German services PMI (March final estimate, 8:55am); Eurozone services PMI (March final estimate, 9am); Eurozone core & headline PPI (Feb, 10am).

Earnings: N/A

Events: N/A

Data: German import price index (Feb, 6am); German factory orders (Feb, 7am); French industrial & manufacturing production (Feb, 7:45am); EZ, French & German construction PMIs (Mar, 8:30am); Eurozone retail sales (Feb, 10am).

Earnings: N/A

Events: Market Holiday – Easter.

Data: N/A

Earnings: N/A

Events: N/A

Data: BRC shop price index (Mar, 12:01am); Nationwide house prices (Mar, 7am); net lending to individuals, consumer credit, mortgage approvals & M4 money supply (Feb, 9:30am); S&P Global manufacturing sector PMI (March final estimate, 9:30am).

Earnings: N/A

Events: N/A

Data: N/A

Earnings: N/A

Events: N/A

Data: New car registrations (Mar, 9am); DMP prices expectations (Mar, 9:30am); S&P Global service sector PMI (March final estimate, 9:30am).

Earnings: N/A

Events: N/A

Data: Halifax house prices (Mar, 7am); S&P Global construction PMI (Mar, 9:30am).

Earnings: N/A

Events: Speech by RBA’s Kent (11:10pm).

Data: Japanese Tankan manufacturing & non-manufacturing indices (Q1, 12:50am); Japanese Jibun Bank manufacturing sector PMI (March final estimate, 1:30am); Chinese Caixin manufacturing sector PMI (Mar, 2:45am); Australian CoreLogic house prices (Mar, 2:01pm); Australian Judo Bank manufacturing sector PMI (March final estimate, 11pm).

Earnings: N/A

Events: RBA minutes of March Policy Meeting (1:30am).

Data: Japanese monetary base (Mar, 12:50am).

Earnings: N/A

Events: N/A

Data: Japanese Jibun Bank service sector PMI (March final estimate, 1:30am); Chinese Caixin service sector PMI (Mar, 2:45am).

Earnings: Kweichow Moutai

Events: Speech by RBA’s Jones (12:50am).

Data: Australian building approvals & private sector houses (Feb, 1:30am).

Earnings: N/A

Events: N/A

Data: Japanese household spending (Feb, 12:30am); Australian trade balance (Feb, 1:30am); Japanese ESRI leading index (February first estimate, 6am).

Earnings: Yaskawa Electric

Extract from Commodity Fundamentals Report No. 178, 28th March 2024:

“Copper: Breakout Underway?”

Longview ‘Tactical’ Alert No. 79, 26th March 2024:

“S&P500: 2013/17 – All over again? a.k.a. Should we expect summer volatility?”

Longview on Friday, 22nd March 2024:

“Tactical & Strategic Asset Allocation Update”

Monthly Commodity Update, 21st March 2024:

“Oil & Aluminium Update: The Bull Case”

Quarterly Asset Allocation No. 57, 20th March 2024:

“Positioning Ahead of a Summer SELL-off”

Longview Letter No. 143, 18th March 2024:

“China: Three Challenging Structural Themes”