Sector Rotation and the Case for Wave Three (More SELLing)

Switch of ‘Global Sector Leadership’ –> Likely Ongoing

By Chris Watling, Global Economist & Chief Market Strategist, Longview Economics

“……..we expect rotation away from the expensive and crowded part of the market,

towards cheap/attractive sectors to persist, particularly as the Fed/other central banks

loosen policy (thereby bringing about a new macro theme)..’”

Source: Longview on Friday, 19th July 2024 - “Rotation & a ‘mini’ UK Boom”, available HERE.

Over the course of this year, we've been writing about the growing case for a change in ‘sector leadership' in the global stock market (for example see HERE and HERE). That expectation (i.e. out of tech/MAG7 and into the cyclical areas of the market) is based on the start of interest rate cutting cycles across the Western world (and the view that the US can achieve a soft landing). As rate cuts begin, market participation should broaden, and cyclicals outperform as the equity market begins to anticipate an upswing in the Western/global economy.

In that sense, July 11th was a critical trading session as the weaker than expected US CPI encouraged the market to price in more rate cuts which, in turn, then drove marked sector rotation (with the NDX down 2% on the day; R2k up 4%). Since then, that pattern of rotation has continued as this pullback has evolved with its ‘wave one’ of selling down to its 5th August lows; then its aggressive ‘wave 2’ relief rally (up until Wednesday); and potentially a ‘wave 3’ of selling (beginning in the past 24 hours - see below).

Indeed, since July 11th US sector rotation has been marked. Defensive areas of the market have rallied and are up around 5 – 10%; cyclical areas are more mixed (as bond yields and the oil price have fallen); while the tech/long duration growth sectors (IT, consumer discretionary and communication services – i.e. dominated by the MAG7) have been the laggards (FIG 1 below).

FIG 1: US sector performance since July 11th 2024 (% return)

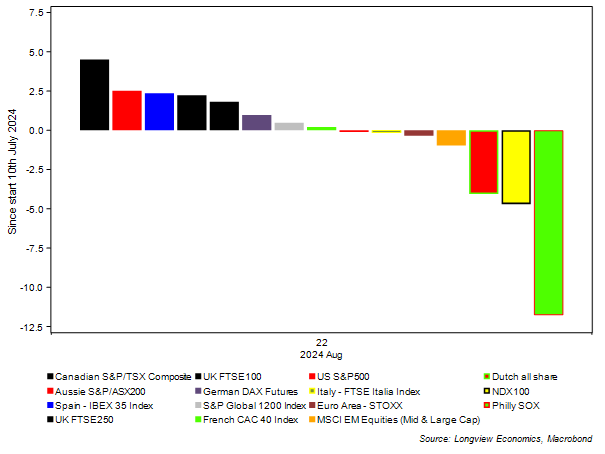

That rotation in US sectors has been mirrored across the globe (i.e. in the performance of key country indices).

Of the key equity indices shown in FIG 2, the NASDAQ & Philly SOX have led the weakness. Within Europe, the Dutch market is the notable (and really only) major underperforming country since July 10th. That reflects its high tech weighting (ASML etc). Taiwan similarly, given its TSMC and tech weighting, has tracked the Philly SOX.

Canadian, Australian, Spanish and UK (both large and mid-cap) equity markets meanwhile, all top the return table since that time, and have generated positive returns (NB these indices are expected to be key beneficiaries of the ‘Great Global Sector Rotation’ theme that we’ve been outlining1. Most of them are either cyclical, or hold some defensive qualities, while exposure to ‘long duration growth stocks’ is low).

While, finally, various other key indices have performed mid-range, often reflecting one-off country specific factors (e.g. like the ongoing French political challenges).

Added to which, the Swiss market is another strongly performing European market (reflecting its defensive characteristics, e.g. high weightings in Nestle, Roche, Novartis etc).

FIG 2: Key country and sector index performances since July 11th

Keep reading with a 7-day free trial

Subscribe to The (Long)View From London to keep reading this post and get 7 days of free access to the full post archives.