The Big Issue

Currently Vexing the Market’s Mind

As always in markets, there are really only a handful of debates which matter. That is, a handful of key issues which, if correctly forecast, will determine the right mix of assets in portfolios, whether at the top ‘global asset allocation’ level (across all asset classes/countries, and indeed often within those asset classes) or at the global equity sector level (and sometimes even single stock).

Critical amongst those key issues, at the moment, are the following questions:

Is Western inflation sticky? Should we worry about the Keynesian Phillips Curve/output gap interpretation about the outlook for inflation (especially in the US)? Or are the Monetarists correct this time?

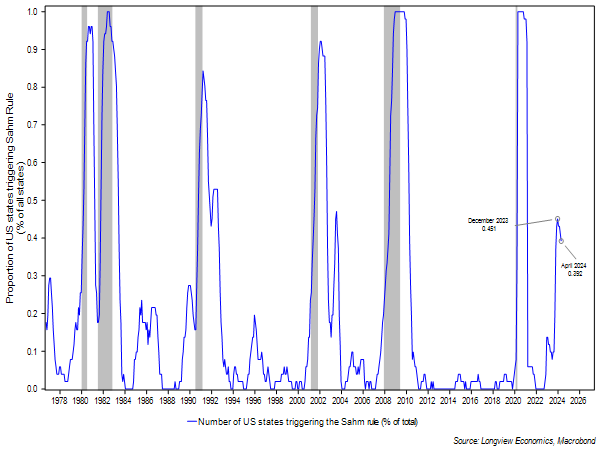

Is US growth going to surprise to the downside? Or indeed is the US about to roll into recession? Should we believe the message of the inverted yield curve (or indeed the Sahm Rule – fig 2)? US recessions, of course (with only one exception in the past hundred years), always bring cyclical bear markets.

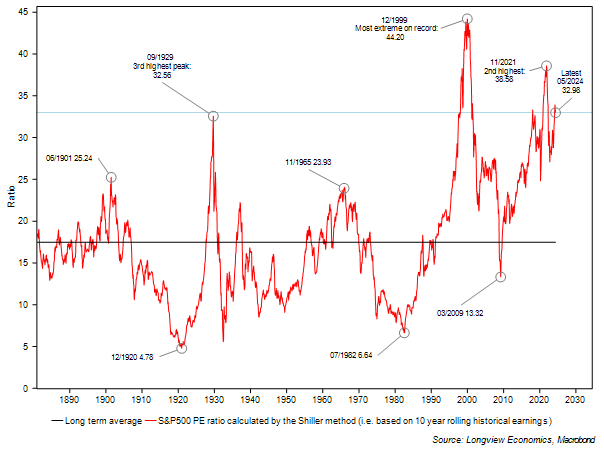

Are the high/rich US stock market valuations a concern? That is, does it matter that the US is currently trading on a 33.0x Shiller PE ratio (i.e. above its 1929 peak – fig 1)? Or is it simply an outdated concept which has been made redundant by the expansion of the Fed’s balance sheet?

Furthermore, is the high concentration risk in portfolios, because of a handful of mega-cap tech stocks, an issue? Or is the real risk that the AI market trend is in its infancy, with the US stock market set to dominate for a few more years (with a repeat of 1999/2000 ahead of us)? Or what about the dominance of passive investing (now substantially above 5o%) – does that create risks?

Is the US exceptional (and therefore still due an above average weighting in portfolios)? Or is it just simply ‘exceptionally profligate’? What does that mean for the dollar – both in a cyclical sense as well as for its ‘reserve currency status’? How does geopolitics interact with the currency (& US bond market)? How should geopolitical risk premiums be priced into risk assets (since with the US market richly priced, it’s difficult to find evidence of a ‘geopolitical’ risk premium in that asset, or indeed in the oil price)? And in that vein, what about the outlook for gold, given geopolitical risks and that Western rate cuts are about to get going, in earnest?

Does it matter that the Fed is still doing QT? Is that about to have an effect on market liquidity, especially given the US Treasury’s announcement about issuing a large amount of debt in Q3? Or has the US Treasury’s ability to manipulate market liquidity (via the use of the TGA, draining the RRP and shifting the duration of their issuance), rendered this less of a concern?

Will the US (& UK) elections matter? If so, how? Does Starmer make much of a difference for markets compared to Sunak? More importantly, what about Trump vs. Biden?

Is there currently an enduring shift in global sector leadership in the stock market? If so, will it last? And what are its implications for investing?

Fig 1: US Shiller cyclically adjusted PE ratio (based on 10 yr rolling EPS)

We’ve written extensively about many of these issues in recent publications. This week, we outlined key views on the prospect for US economic growth, thinking about “How High is US Recession Risk? Is Growth Slowing? Have the US & EU Decoupled?” – (contact Nick Beazley for a copy of the full report).

In conclusion:

“Given the softening labour market, the US fiscal tightening in 2024 (which we outlined in the ‘Longview on Friday’ published 3rd May 2024), coupled with the low household savings ratio and still tight monetary policy, we expect US growth to disappoint in 2024 (relative to consensus).

Reflecting the ‘Key Points’ laid out above, though – and the underlying structural balance sheet and corporate sector strength – we don’t expect a US recession in 2024. Indeed we retain the probability at 20% (for this year), as a reflection of the softening labour market and still contracting LEIs, but we haven’t increased it from that level.”

Source: Longview Economics, Global Macro Report, 22nd May 2024

In recent (Long)View from London publications, we considered the issue of “How Exceptional is America?” (see HERE). As part of that, we analysed the fiscal situation in 2024 and outlined the fiscal tightening that is occurring this year (see HERE). The liquidity risks were addressed in previous Tactical Equity Asset Allocation publications. US inflation was touched upon in this recent publication (HERE or HERE); while the rich US valuations and shifting global sector leadership have been outlined/looked at HERE & HERE.

Below we dig further into the ‘sticky inflation’ issue, given that both the UK & Japan have reported their latest inflation data this week – whilst the RBNZ & RBA both discussed possibly raising rates one more time (earlier this week – e.g. RBNZ’s Orr: “Raising rates was a real consideration”, “policy committee discussed possibility of raising rates”, 22nd May 2024 & Australia’s “RBA Resumes Rate-Hike Talk on Renewed Inflation Concerns” – available HERE). Below that, and given that the UK election was called this week (with an election date of July 4th), we look at the implications for the economy and UK stock market, if Labour win.

Fig 2: Proportion of US States triggering the Sahm rule1 (% of total)

UK Data –> Troubling Trends? Or Just April Seasonality?

Keep reading with a 7-day free trial

Subscribe to The (Long)View From London to keep reading this post and get 7 days of free access to the full post archives.